- 0 – Introduction

- 1 – Web3 User Journey

- 1.1 – Onboard to Exchange & Purchase Crypto

- 1.2 – Create Web3 Wallet & Receive Crypto

- 1.3 – Manage Crypto from Wallet

- 1.4 – Connect wallet & access Web3 ecosystem

- 1.5 – Web3 wallets and cryptographic keys

- 1.6 – Introduction to decentralized, P2P blockchain networks

- 1.7 – Sending transactions to the blockchain

- 1.8 – Interacting with dApps on the blockchain

- 2 – Evolution of Blockchain Ecosystems

- 3 – Web3 Tokens as Incentive Mechanisms

- 4 – Decentralized Finance (DeFi)

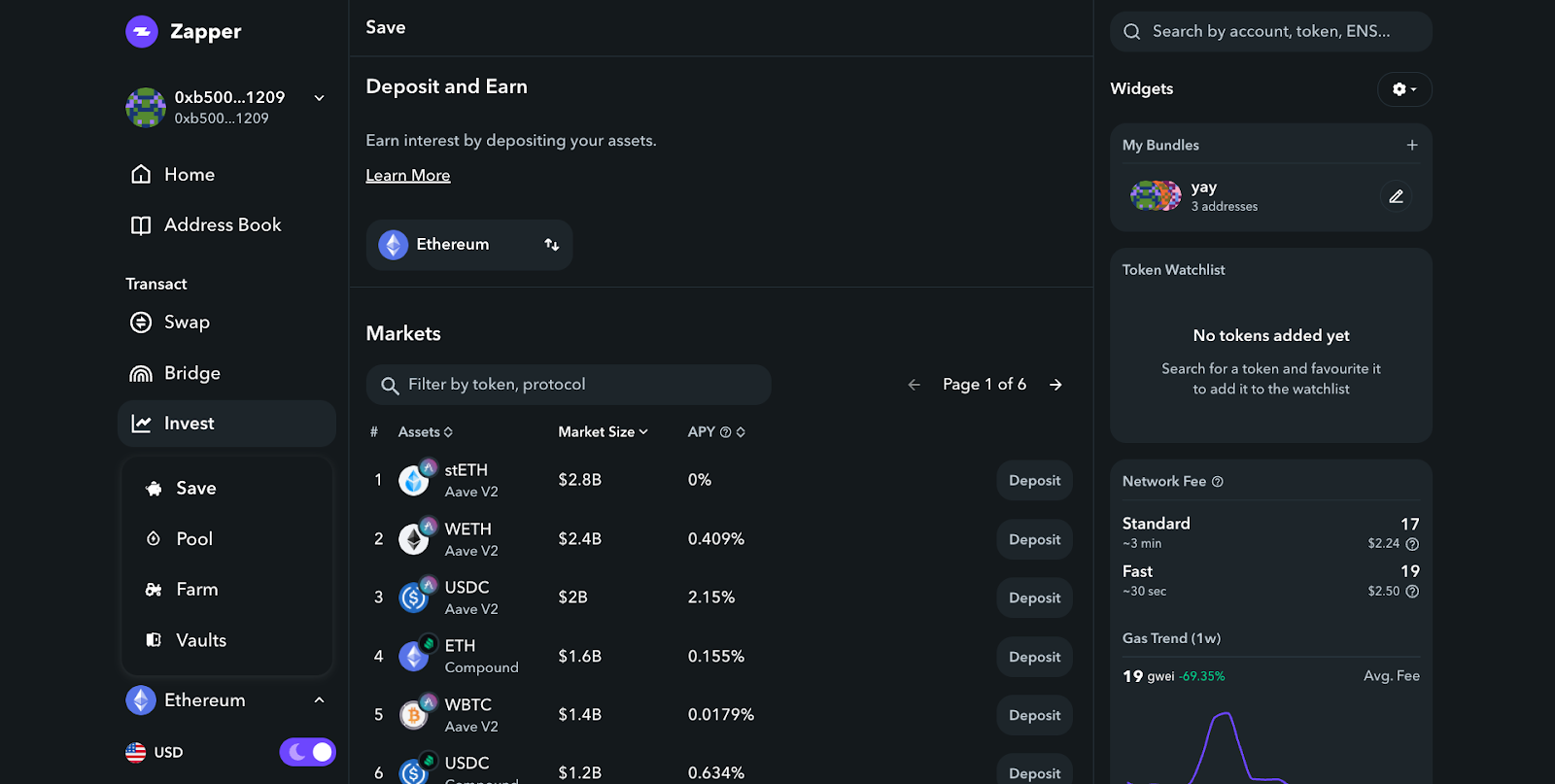

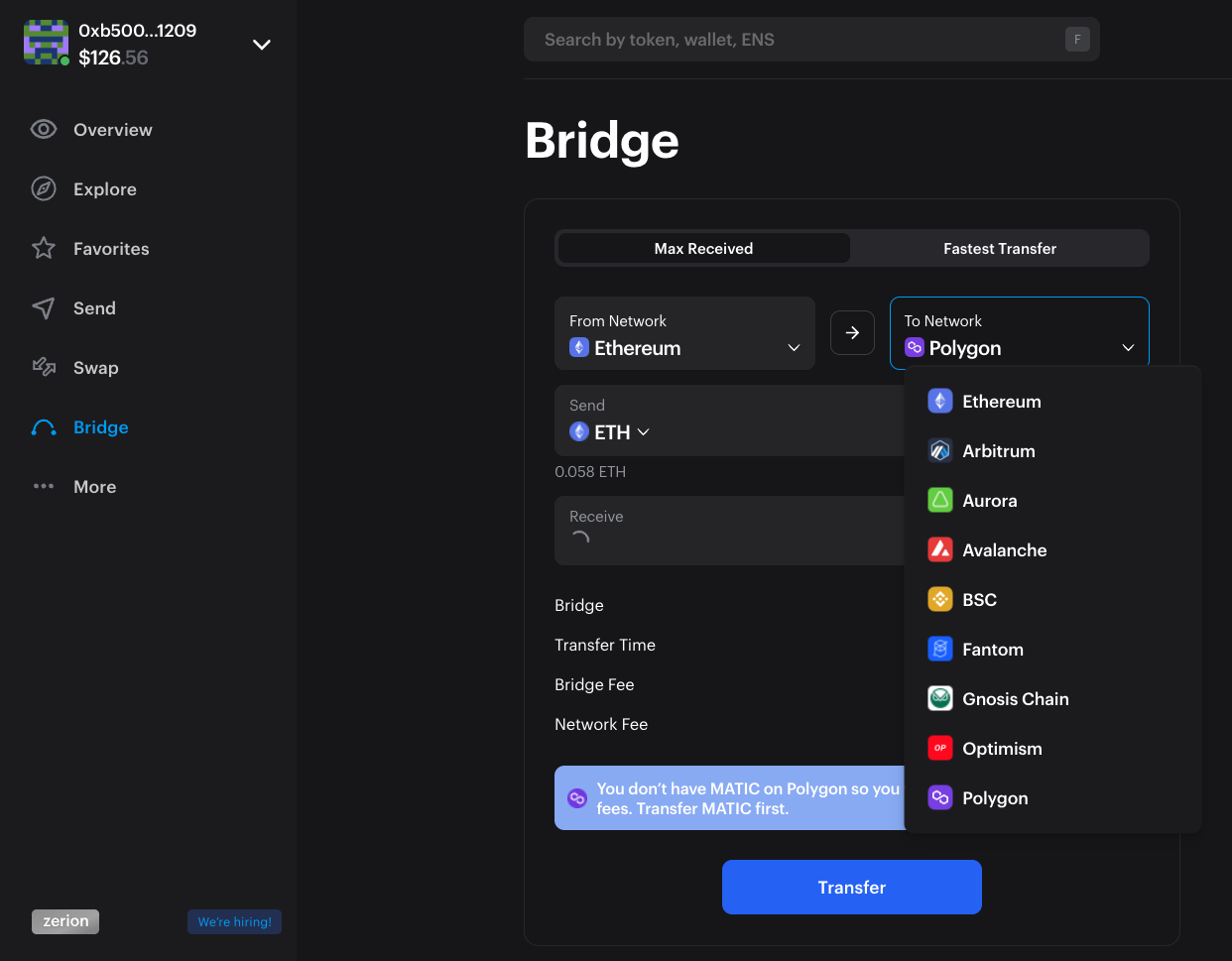

- 4.1 – Swap tokens with Uniswap

- 4.2 – Mint stablecoins with MakerDAO

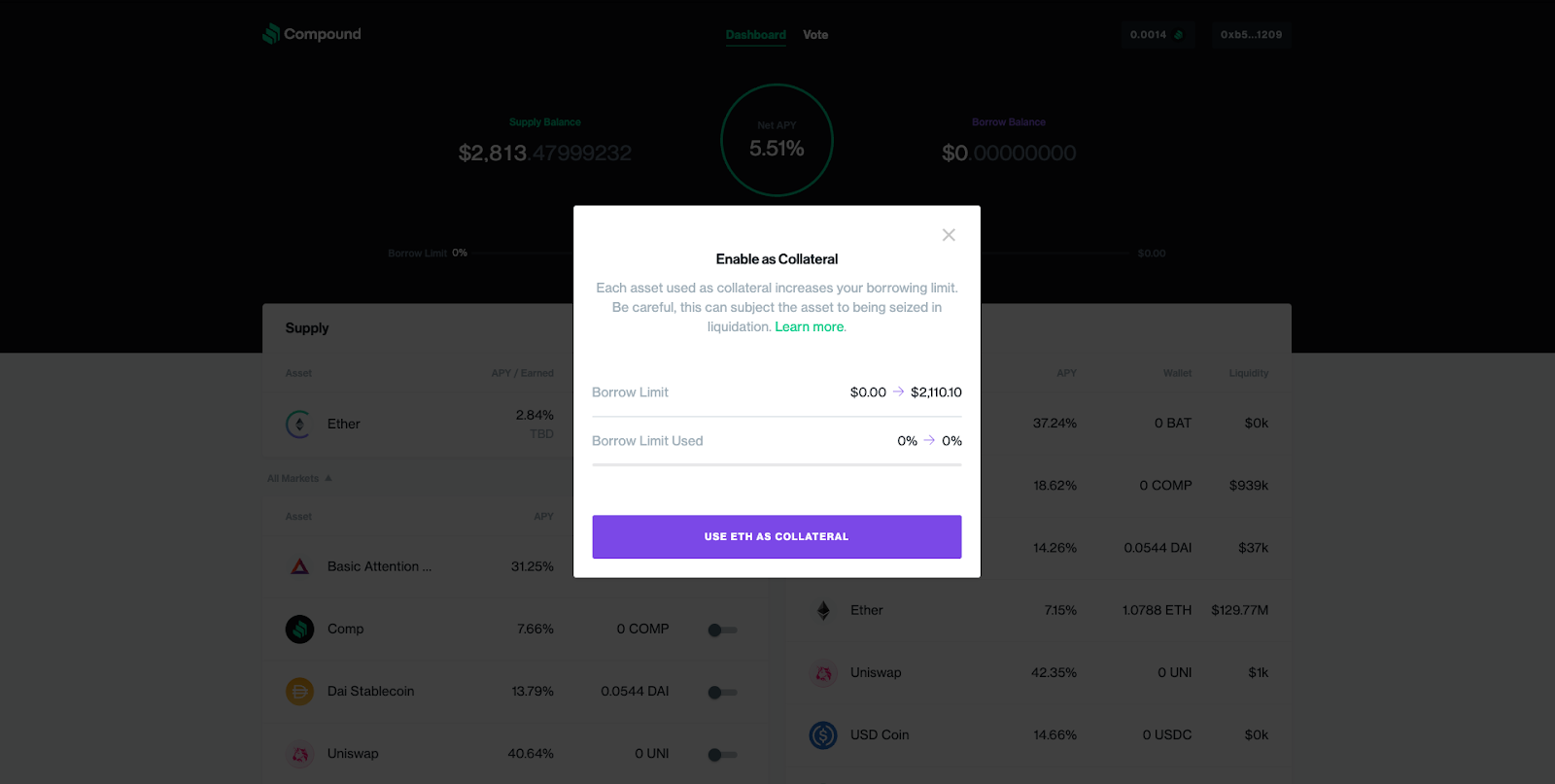

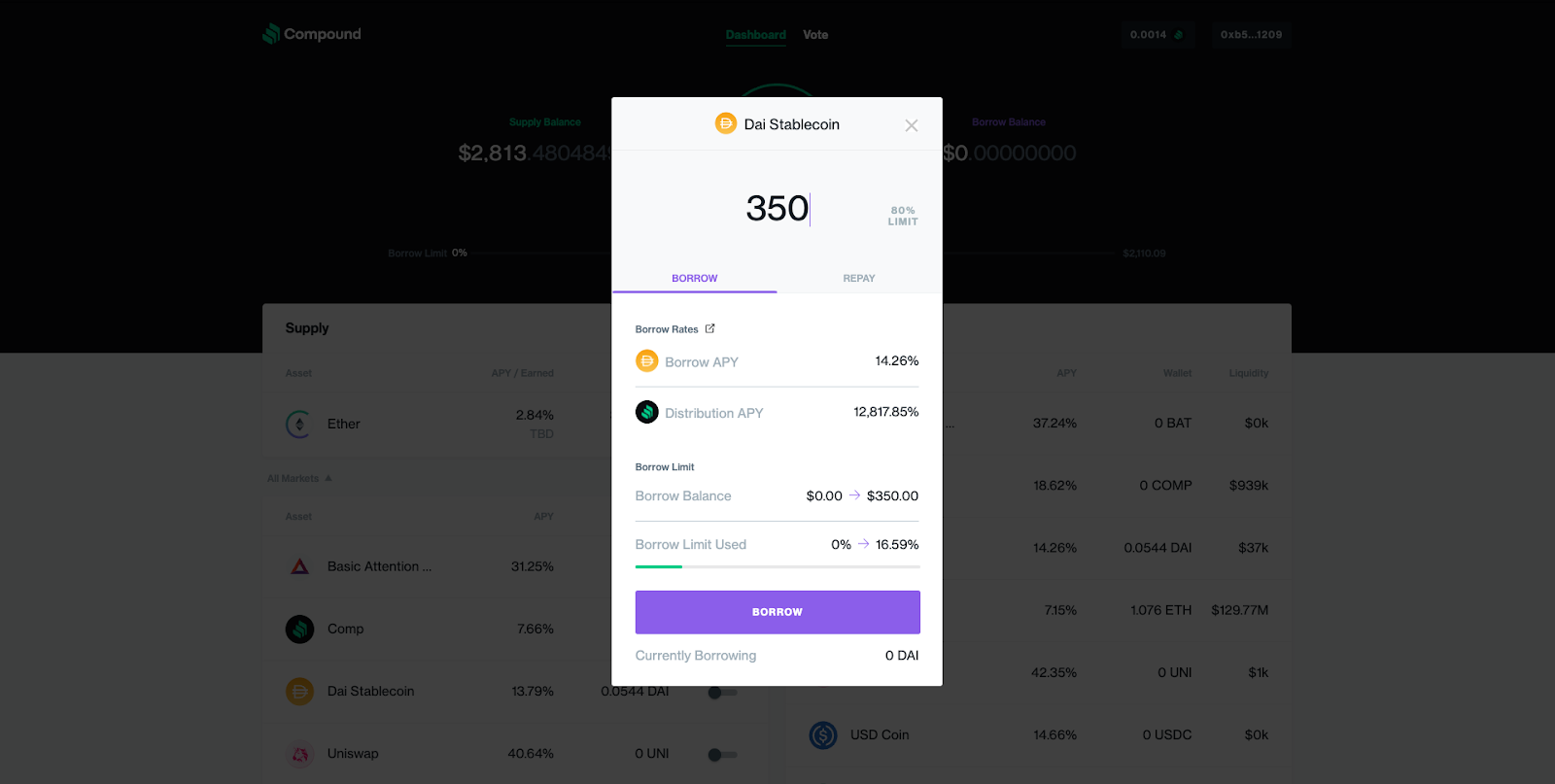

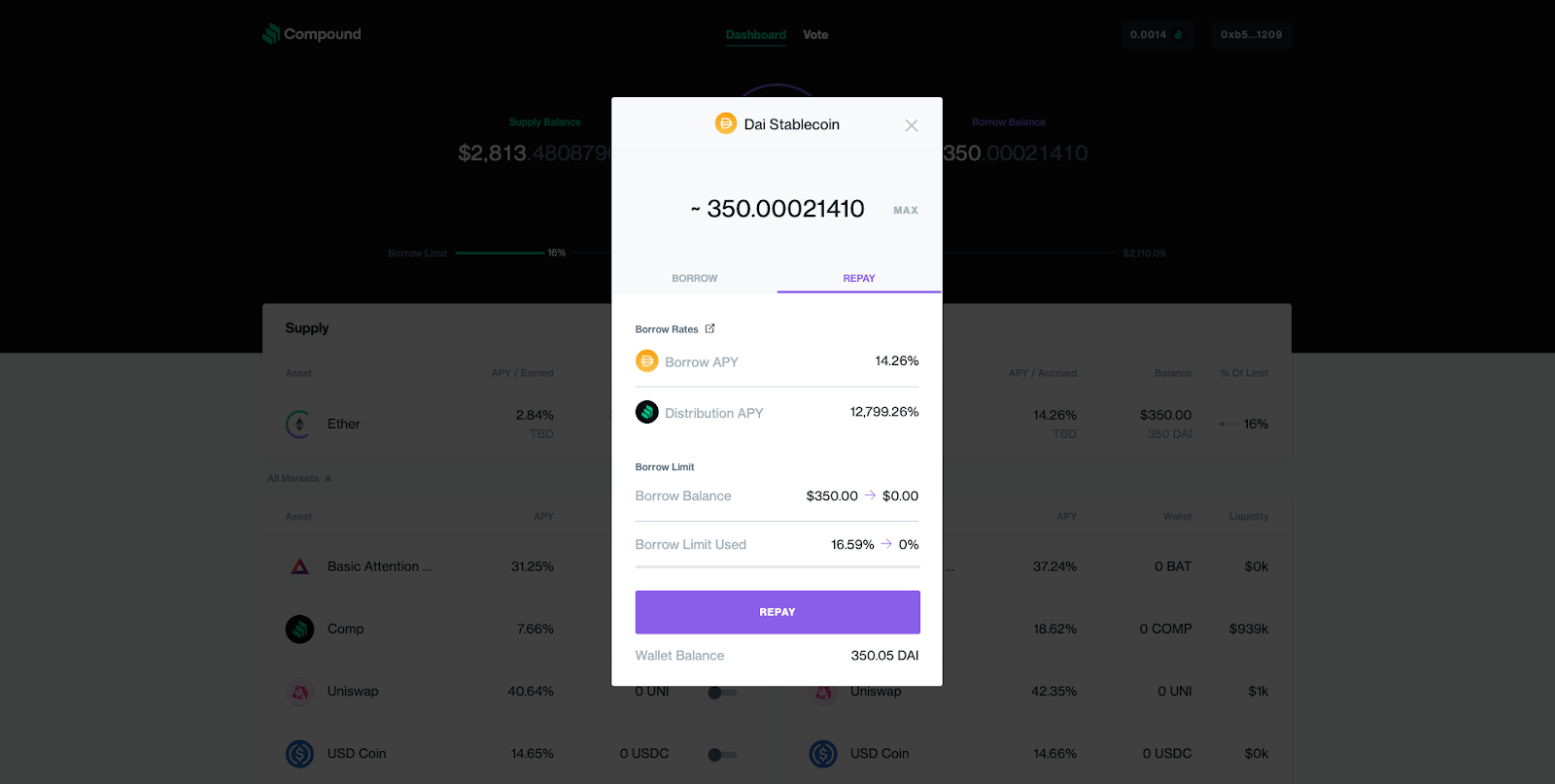

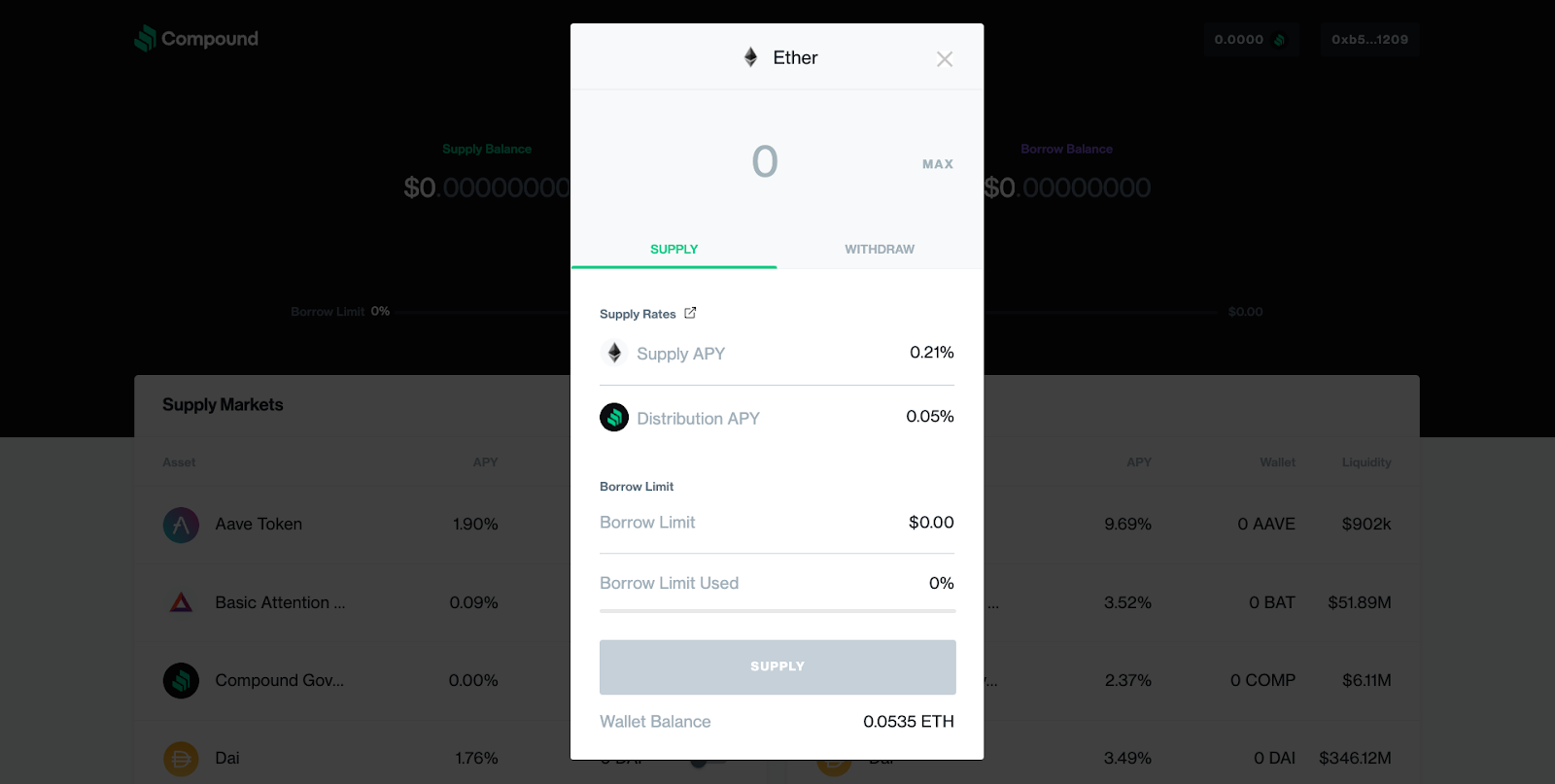

- 4.3 – Lend crypto with Compound Finance

- 4.4 – Liquidity mining to boost yield

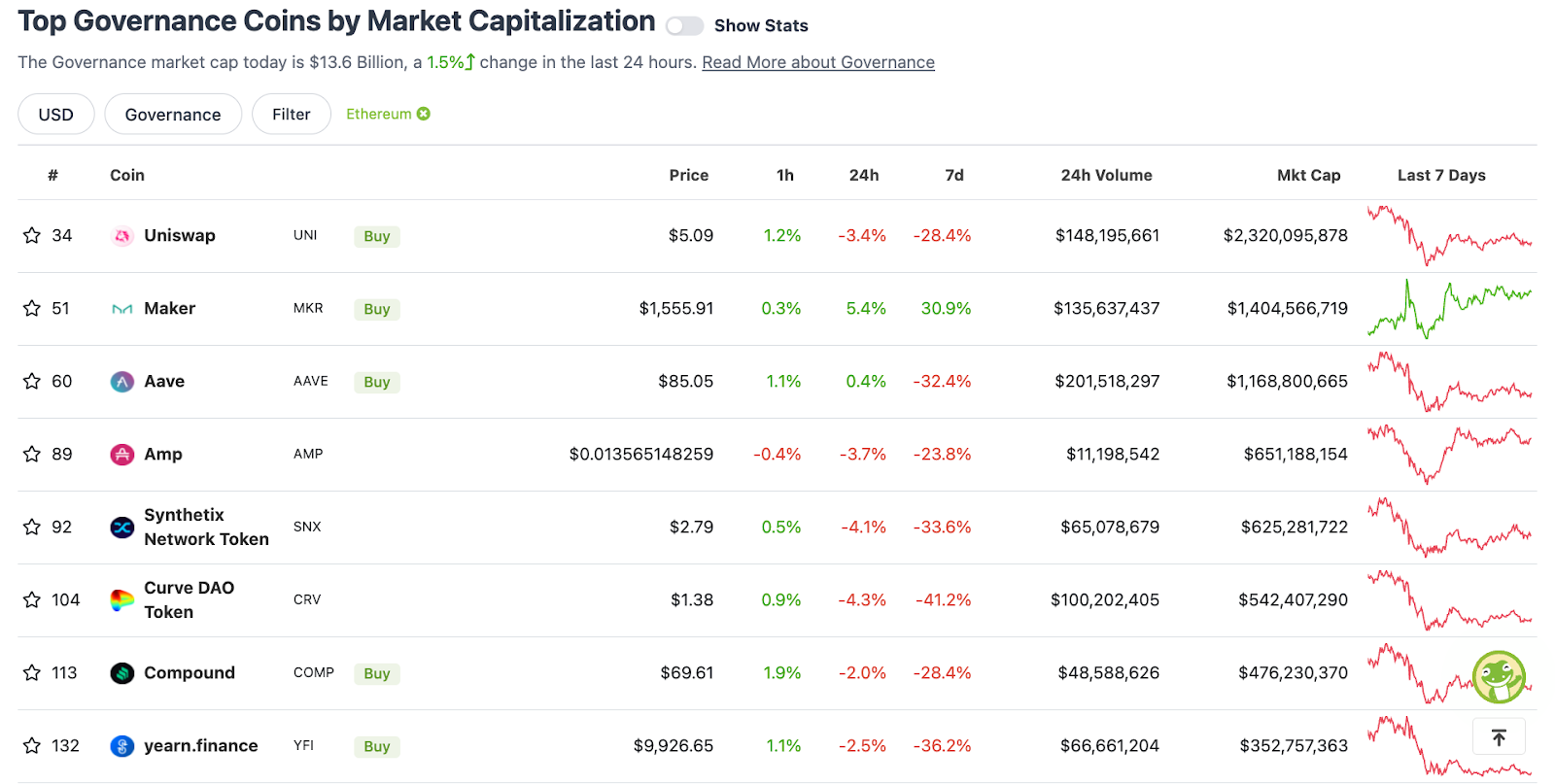

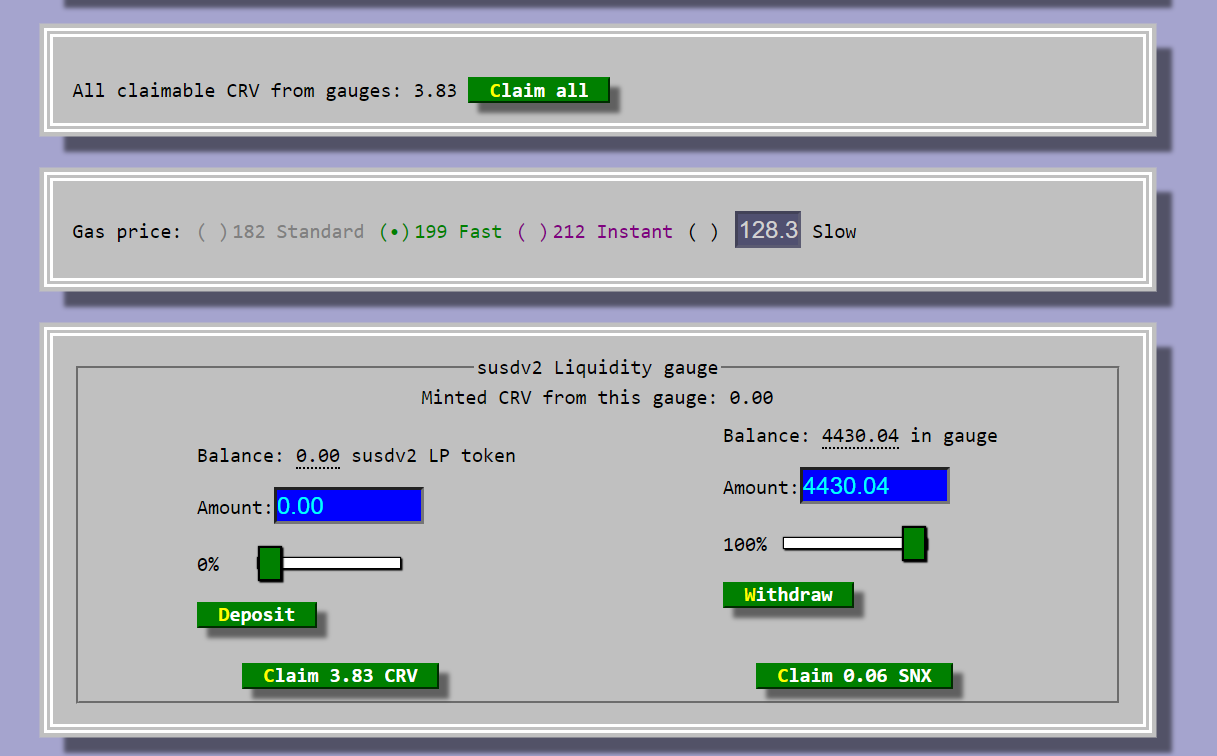

- 4.5 – Yield farming with Curve Finance

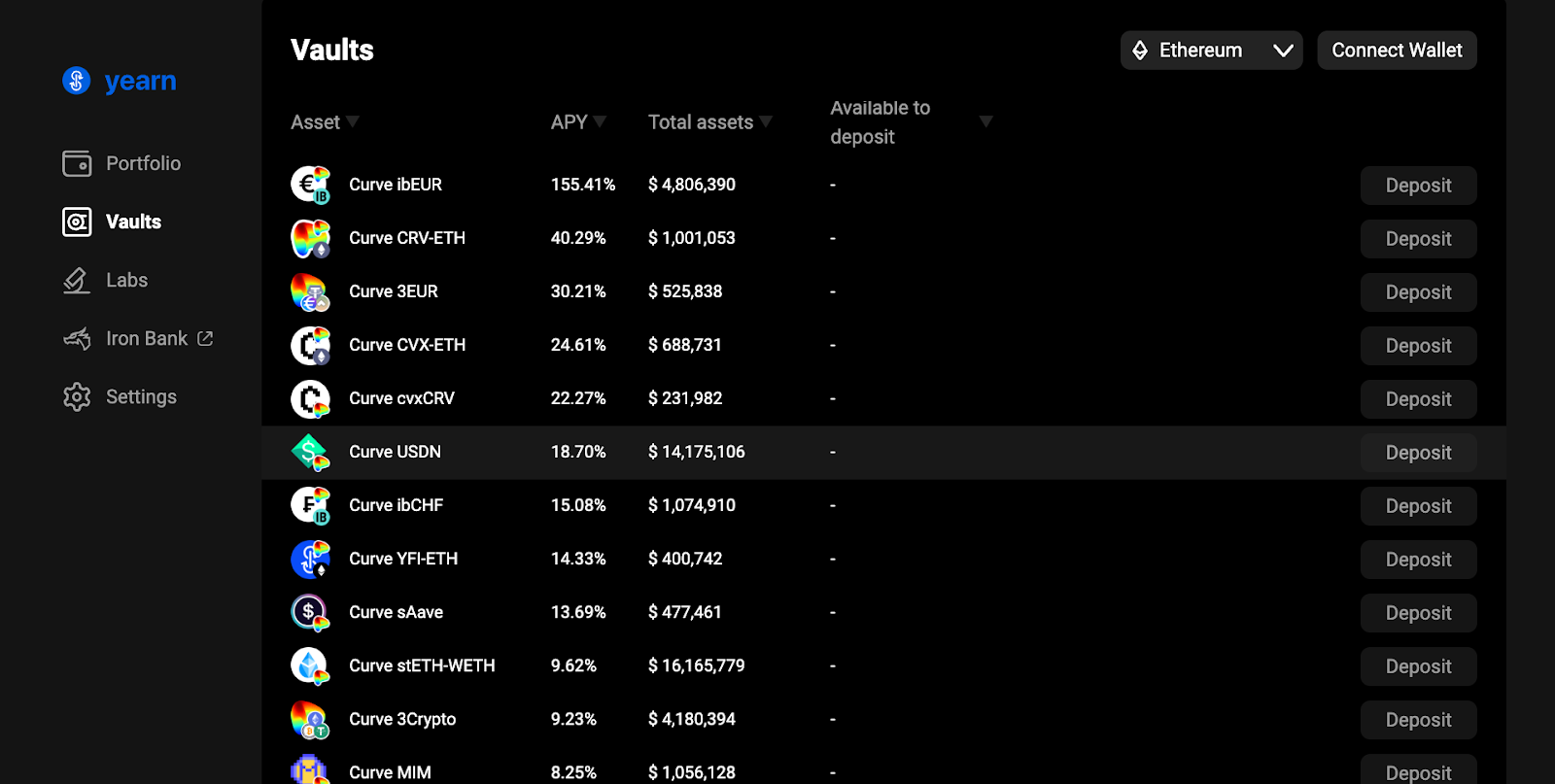

- 4.6 – Automated investing with Yearn Finance

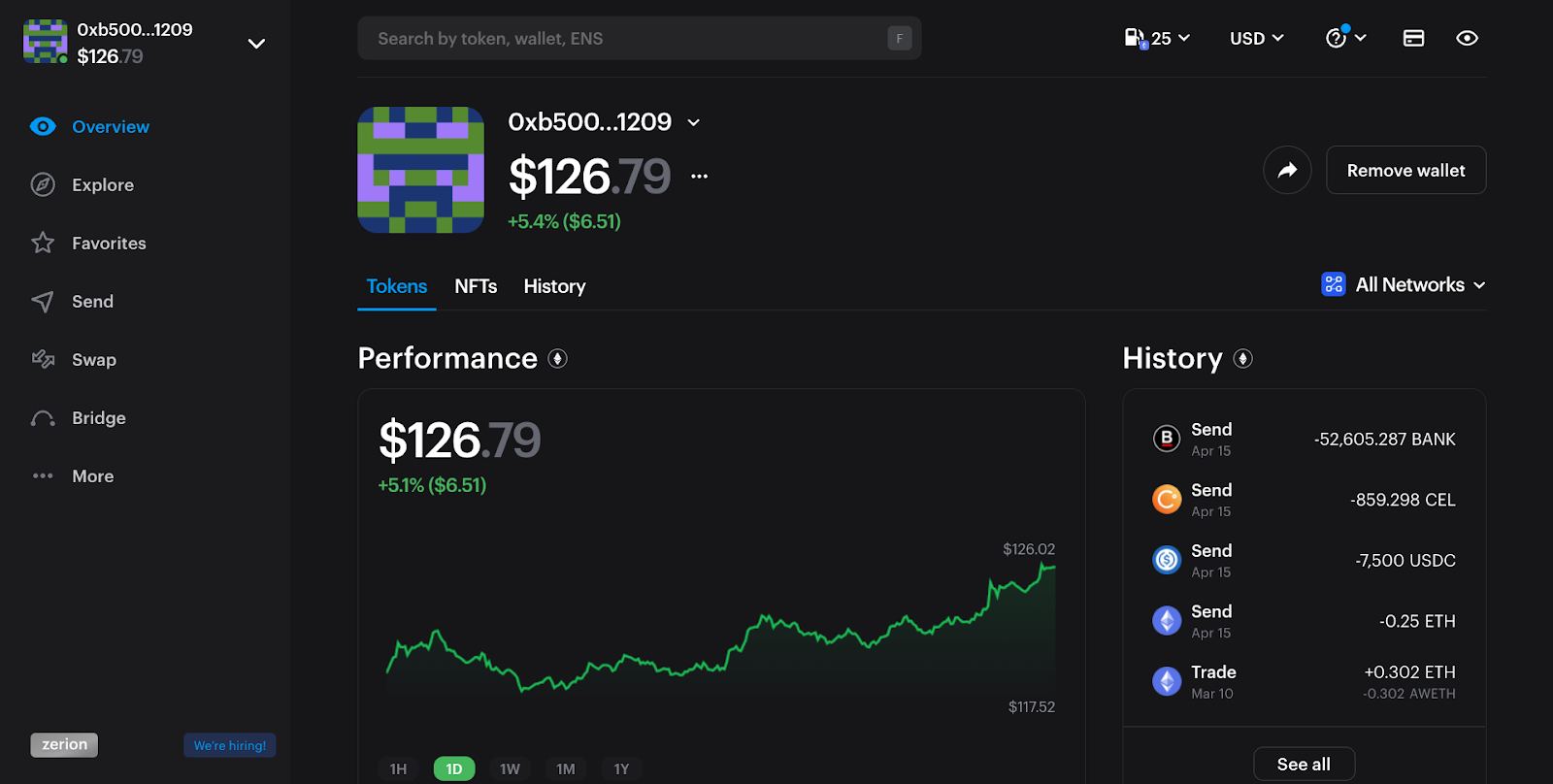

- 4.7 – DeFi dashboard with Zerion

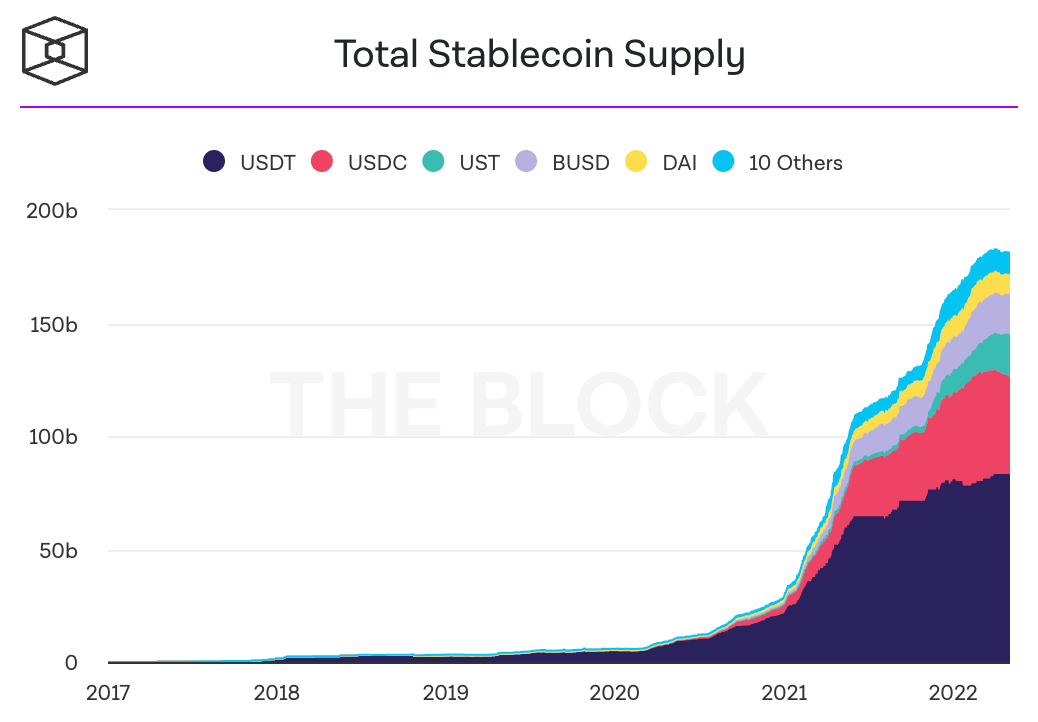

- 4.8 – DeFi 2.0 & Stablecoin Wars

- 4.9 – Deep liquidity with OlympusDAO

- 5 – Cryptomedia and NFTs for Web3 Creatives

- 6 – Decentralized Web Infrastructure

- 7 – Self-Sovereign Identity

- 8 – Decentralized Social Media and DAOs

- 9 – Decentralized Gaming and the Open Metaverse

0 – Introduction

Web3 extends human rights into the digital realm. Web3 users are empowered with the Right to Digital Privacy, Property and Inclusion. Digital privacy is about users controlling their own application data, digital property about the ability to own and custody scarce digital assets, and digital inclusion about guaranteed access to the digital economy and society with permisionless internet services.

And this is all without the trust in, or permission from, central authorities like governments, institutions, and companies. Right now we only have the appearance of these digital rights; and, in actuality, must trust these central authorities to act in our best interests, and preserve our rights for us. But our digital rights are infringed on constantly.

Our lives are moving more and more into the digital realm. Billions of people interact with digital technologies on a daily basis, but we still rely on central authorities to give us access to these internet services and our application data. Web3 secures our rights in these digital worlds, and puts more power into the hands of the individual.

1 – Web3 User Journey

This chapter is structured as a user journey for onboarding to Web3. Going step-by-step through this journey will show you the UX of decentralized applications (dApps), and help in building empathy for Web3 users in general.

It starts when users connect their bank account to a crypto exchange, and purchase cryptocurrency. A large emphasis is placed on this step – it’s known as the “on-ramp” to cryptocurrencies. Users exchange their fiat currencies (e.g. USD) for cryptocurrencies (e.g. ETH). The UX for purchasing crypto differs between exchanges, but significant friction points are present on all of them.

The cryptocurrency that users purchase on an exchange is being custodied by that exchange. Users must self-custody their crypto in order to take full advantage of the Web3 ecosystem, and its decentralized applications. Users first create a Web3 wallet then send crypto from the exchange to the wallet. This marks an important transition from using centralized products (i.e. banks and exchanges) to using decentralized, blockchain-based products (i.e. wallets and dApps).

Web3 wallets can be thought of as anonymous bank vaults. Anyone can create one, and users don’t need to reveal their identity (unlike banks and exchanges) in order to do so. Within Web3 wallets, users manage their crypto assets like checking token balances, and sending crypto to other wallets.

Finally, wallets are connected to decentralized applications (i.e. dApps). This is how users access the Web3 ecosystem. Web3 dApps are distinctly different from the Web2 applications we’re accustomed to using (e.g. Facebook and Twitter). Decentralized applications are built on top of blockchains, rather than centrally-managed servers and databases. The dApp ecosystem is experiencing rapid growth, and new categories of Web3 products are being built out, like decentralized social media, data, identity, gaming, and much more.

So that’s an overview of the Web3 user journey. In the sections that follow, we’ll go more in-depth on each one of the four phases. After discussing the phases, we will touch on more advanced concepts like what a Web3 wallet is on the backend, what is a blockchain and P2P network, and how Web2 apps differ from Web3 dApps in terms of software architecture. By the end, you’ll have a solid understanding of Web3 concepts, design patterns, and the underlying blockchain technologies.

1.1 – Onboard to Exchange & Purchase Crypto

Crypto is the currency of the Web3 ecosystem, and is required to access decentralized applications. So how do users first get cryptocurrency? This is where crypto exchanges come in.

Exchanges are known as the “on-ramp” to cryptocurrency, because it’s where users convert their fiat currencies into cryptocurrencies. Let’s talk about the user journey for onboarding to crypto exchanges, and purchasing cryptocurrency on them. Product designers put a large emphasis on crypto exchange onboarding, because the UX has been bad in the past and user friction still exists today.

Before writing this, I onboarded to four crypto exchanges (Coinbase, Kraken, Crypto.com, and Gemini), and tested the user experience of each. Coinbase by far had the best UX of all crypto exchanges I looked at. It’s one of the most mature Web3 companies as it has been running since 2012, it went public in 2021, and it continues to build a robust team of UX designers and researchers. In my opinion, Coinbase is the gold standard of crypto exchange UX at this time.

Before we get into the specifics, understand that the user flow is broken into four phases on all exchanges: sign-up to the exchange, verify your identity to meet government KYC/AML requirements, transfer funds from your bank account to the exchange, and, finally, purchase crypto.

Sign-up is similar to other web services. The user creates an account with an email username, and sets a password. They receive email verification, and text verification for 2FA. Nothing abnormal yet.

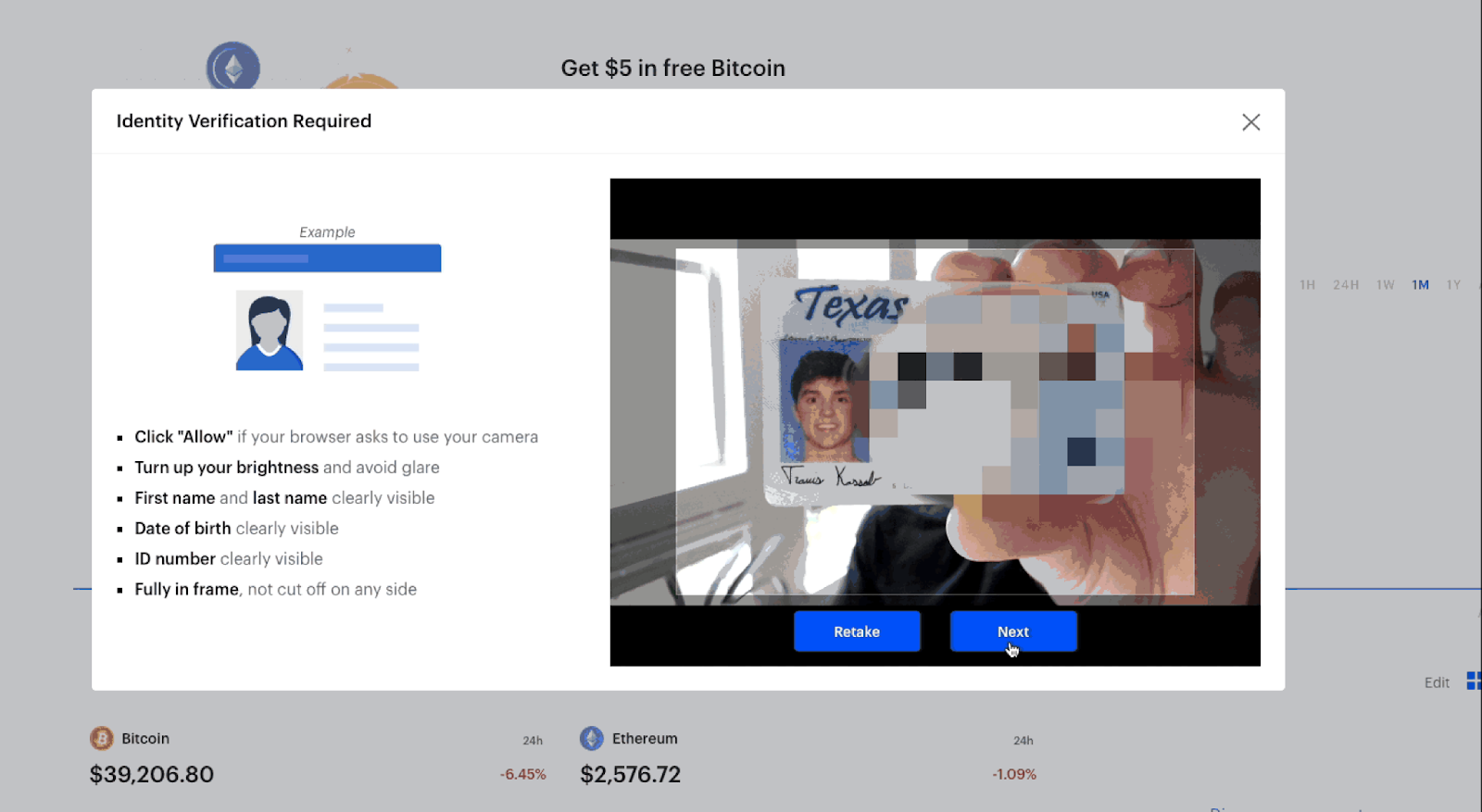

The UX starts to degrade in the next step where the user must verify their account. In other words, the user must prove their identity using government issued documents (i.e. passports, drivers licenses) in order to use the exchange. This account verification has to do with the exchange complying with KYC (Know-Your-Customer) and AML (Anti-Money Laundering) regulation. Basically, the exchange is considered a bank, and governments want to control who has access to these banking services.

Most would agree that we shouldn’t let terrorists, criminals, and other sanctioned individuals use banking services; however, for the average user, this account verification step poses a couple problems. First, account verification requires the collection of sensitive information like residential address, social security number, and government-issued documents (e.g. passports and driver’s licenses). I think we all know privacy-conscious people who wouldn’t feel comfortable providing this information to a crypto exchange, and submitting it over the internet for that matter. Looking at you mom and dad.

Also, users are not told how long the account verification process will take. Admittedly, it only took one minute for me to receive a confirmation email from Coinbase, but this could still prevent people from setting up an account and purchasing crypto all in one sitting. Kraken and Crypto.com took 5-10 minutes for account verification. My account verification on Gemini is still pending, over 6 months later.

Now, the next step in this journey is for users to connect their traditional bank account to the crypto exchange. This has to do with landing fiat currency into the crypto exchange so that it is available to purchase the cryptocurrency with. Exchanges provide a variety of transfer methods, such as ACH transfer, Bank Wires, PayPal, and Debit cards. These methods differ in terms of transfer limits, transfer fees, and how long it takes to land fiat in the account.

Coinbase integrates with a third-party service called Plaid to make the ACH transfer process more user-friendly. Connecting my bank to Coinbase via Plaid took only 30 seconds, and I was ready to purchase cryptocurrency from there. This is where Coinbase really starts to set itself apart from the others. When using the other exchanges, I was forced to open a new browser tab, log into my bank account and manually initiate bank wire transfers into the exchange. I was not charged any fees; however, the funds took 24-48 hours to land in the exchange. You can imagine how much more this disrupts the user flow compared to Coinbase’s seamless ACH transfer.

Finally, once fiat has landed in the exchange, the user is able to purchase cryptocurrency. It’s a simple process on all exchanges. The user selects which cryptocurrency they want to purchase and how much of it, denominated in their fiat currency.

That’s a summary of what happens on a crypto exchange, and we highlighted some major friction points along the way. Next, we’re going to talk about Web3 wallets, look at the process of creating one, and sending crypto from the exchange into the wallet. This is where we bridge the gap between Web2 and Web3, this is where we go from centralized custody to decentralized, self-custody.

1.2 – Create Web3 Wallet & Receive Crypto

Now that we have crypto in our exchange account, we’ll want to create a Web3 wallet so that we can move our crypto from the exchange into the wallet. This is where the world of Web3 decentralization begins, and there’s a lot that will be new here for first-time Web3 users. Let’s start by creating a wallet with the most popular crypto wallet app, MetaMask.

MetaMask is a Chrome browser extension that can be downloaded through the Google extension store. There are other types of wallets like desktop and mobile apps, but browser extensions are the most popular form factor for Web3 wallets. Let’s now look at the process for creating a Web3 wallet.

First, users need to install the MetaMask extension on their Chrome browser. Clicking on the MetaMask extension will launch an onboarding screen for MetaMask, and there are two user flows from here: create new wallet and import existing wallet. The ladder has to do with recovering a wallet, which we’ll look at later. For now, we will create a new wallet.

MetaMask generates a new wallet, and displays something called a “secret recovery phrase” for the user to copy. The secret recovery phrase is a series of 12 to 24 everyday words, and is the master password for the Web3 wallet. Anyone with this phrase can import the wallet into their MetaMask application, and access the crypto associated with the wallet. Users usually write this down on a physical piece of paper, and store it somewhere safe (like a safety deposit box) for security reasons. On the next screen, MetaMask requires the user to retype the secret recovery phrase to ensure the user copied it down correctly in the first place.

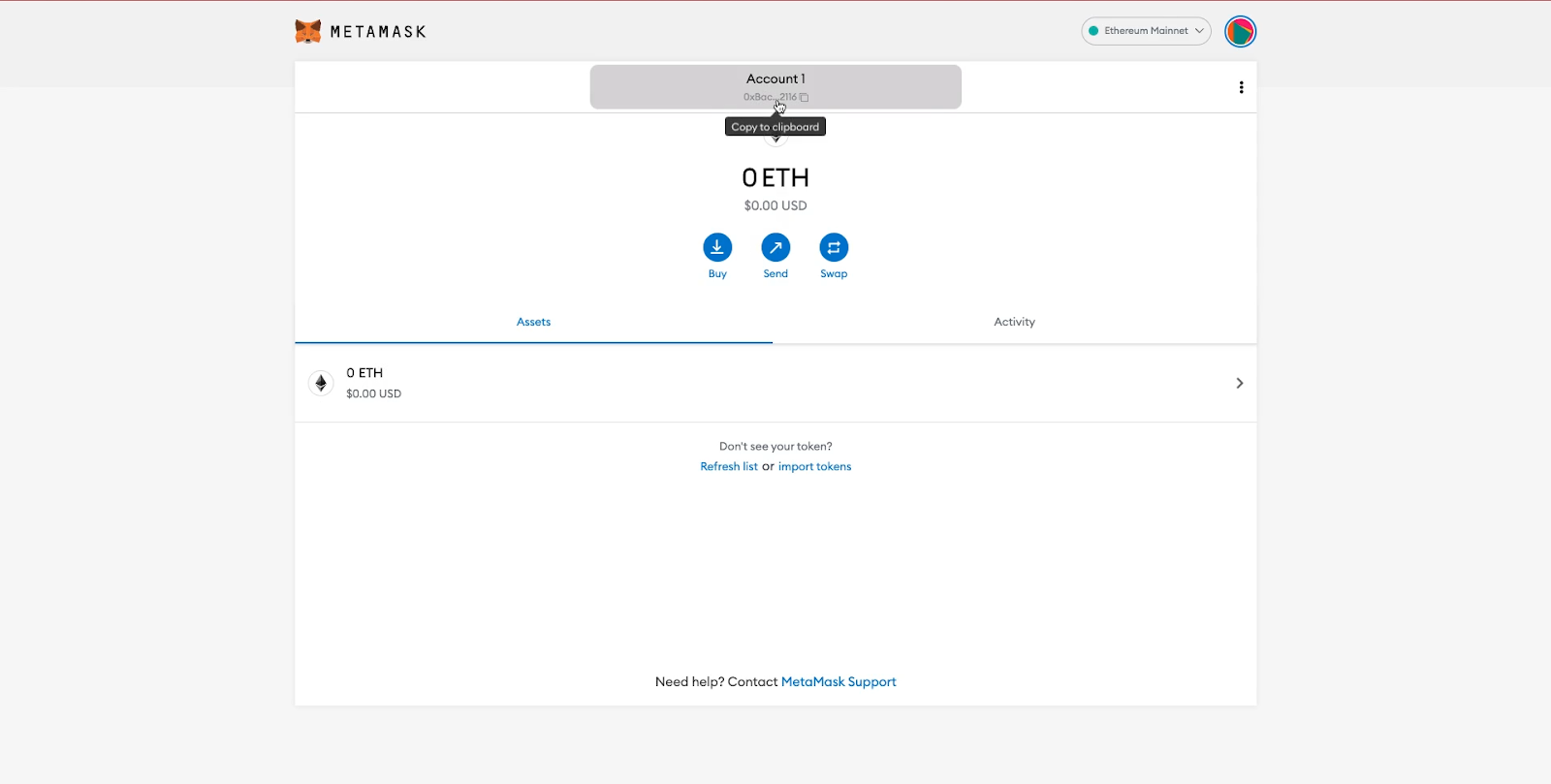

Users can access the wallet’s main UI once the secret recovery phrase has been backed-up. The next section goes in-depth on the features and design patterns of a Web3 wallet, but for now we will just look at the wallet’s address in the top center of the UI. The address is a unique, public identifier for the wallet, and we copy it to our clipboard in order to send crypto from the exchange into the wallet. You can think of the wallet address like an email address. Remember, sending crypto from the exchange to the wallet is an important transitory step to go from centralized apps to decentralized apps.

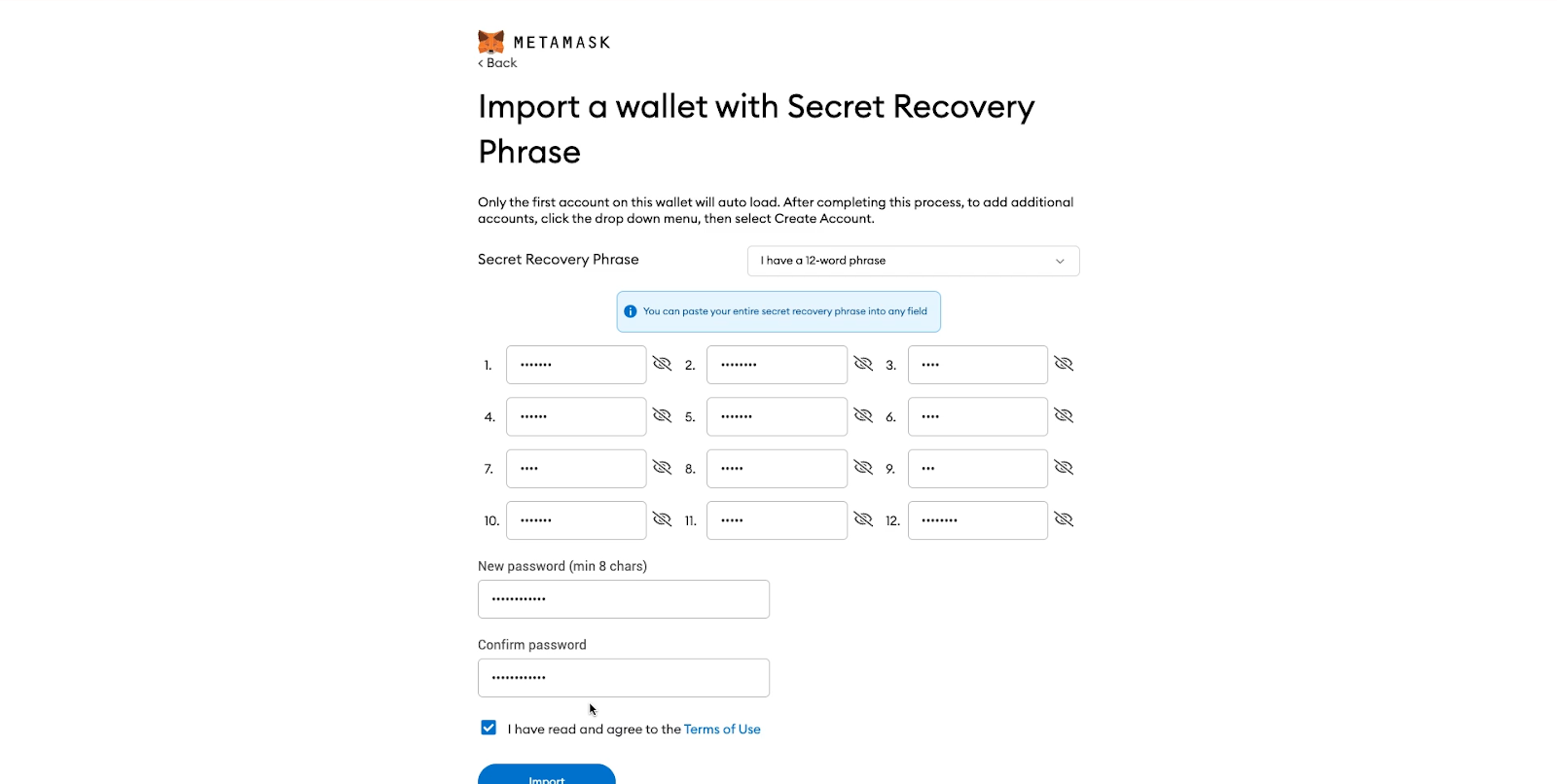

Now, let’s say you change computers, and need to redownload MetaMask. Or your MetaMask extension gets deleted from Chrome. In order to regain access to your wallet, you’ll need to recover your wallet using your secret backup phrase. Let’s see how this works by going back to the initial MetaMask onboarding screen, and importing an existing wallet. The user simply enters the secret recovery phrase, and their Web3 wallet gets imported into the fresh MetaMask app.

Now that we’ve seen how to create a wallet, send crypto to it, and recover the wallet – let’s talk about some common pain points related to Web3 wallets, and why they are intimidating, especially for first-time users. When signing up to your traditional bank, you set your username and password. This username and password exists in your bank’s private database so, if you lose your password, you can initiate a password reset process to regain access to your account. On the other hand, Web3 wallets represent decentralized, self-custody bank accounts. This means no centralized entity custodies your crypto, or manages your account information.

The main implication here is that, if you lose your secret recovery phrase, you lose access to your crypto funds forever, without recourse. There is no centralized service that will help you recover your funds. Imagine you are in custody of gold bars – you are the sole person responsible for remembering where you buried the gold. Losing your secret recovery phrase is the equivalent of forgetting where you buried your gold bars. Self-custody demands a significant amount of responsibility from Web3 users, but some wallets are working to improve this pain point with something called social recovery.

Also, Web3 wallet transactions are irreversible. If you type in your friend’s address wrong, or accidentally send crypto to the wrong person, then the transaction cannot be reversed. Also, if your wallet gets hacked, and the crypto gets drained from it, there’s no recovery process for getting your funds back.

Web3 wallets are a permanent fixture in the Web3 ecosystem. The user will continuously return back to their wallet’s UI to manage their crypto assets, and connect their wallet to decentralized apps. Also, we go in-depth on one of the most common user flows within a Web3 wallet: sending crypto to other wallets.

1.3 – Manage Crypto from Wallet

Wallets are central to using the Web3 ecosystem – users continuously return back to wallets in order to view their account balances, and send crypto to other wallets. Before we get into these features, let’s talk about the properties of Web3 wallets.

First, Web3 wallet’s are “permissionless” bank accounts. They are permissionless because anyone can download, create, and use a wallet without the permission of an authority like a government or bank. Also, Web3 wallets are “anonymous” bank accounts. Unlike traditional bank accounts, Web3 wallets do not require identity verification. Finally, Web3 wallets are “censorship-resistant”. Recently, we’ve seen governments freeze the bank funds of its citizens. This cannot be done with cryptocurrency managed by Web3 wallets.

As a side note, Web3 wallets are actually much more than a bank account. Their most obvious function is to custody cryptocurrency, but Web3 wallets also hold other digital items like artwork (i.e. NFTs), and will eventually be used to manage user data, identity, and more.

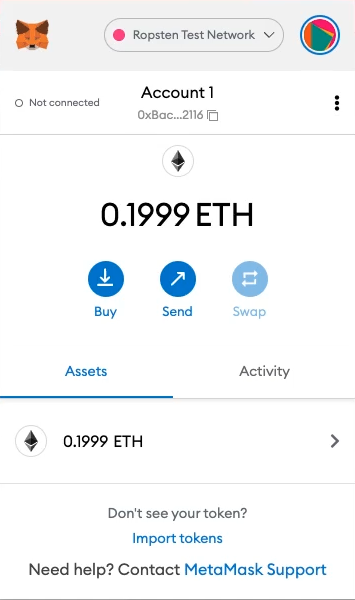

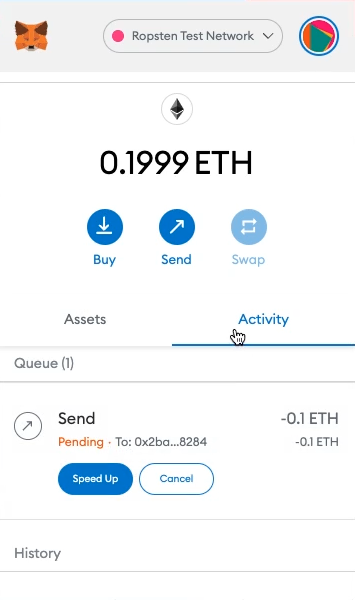

Now let’s briefly talk about the features within a Web3 wallet. Of course users can check their account balance at the top, which shows how much ETH is in the wallet. Wallets can hold other tokens in the “Assets” tab. The “Activity” tab on the right shows a history of the incoming and outgoing transactions associated with the wallet. At the top middle is the “Account”, which users click in order to copy the wallet address to their clipboard. Just above “Account” is the “Network” where users can change blockchain networks. MetaMask is connected to “Ropsten”, an Ethereum testnet blockchain, in the image above. Developers use testnets to debug their apps before deploying to “Ethereum Mainnet”. Finally, to the left of “Account” there is a “Not connected” button. This UI element turns green when the wallet is connected to a dApp.

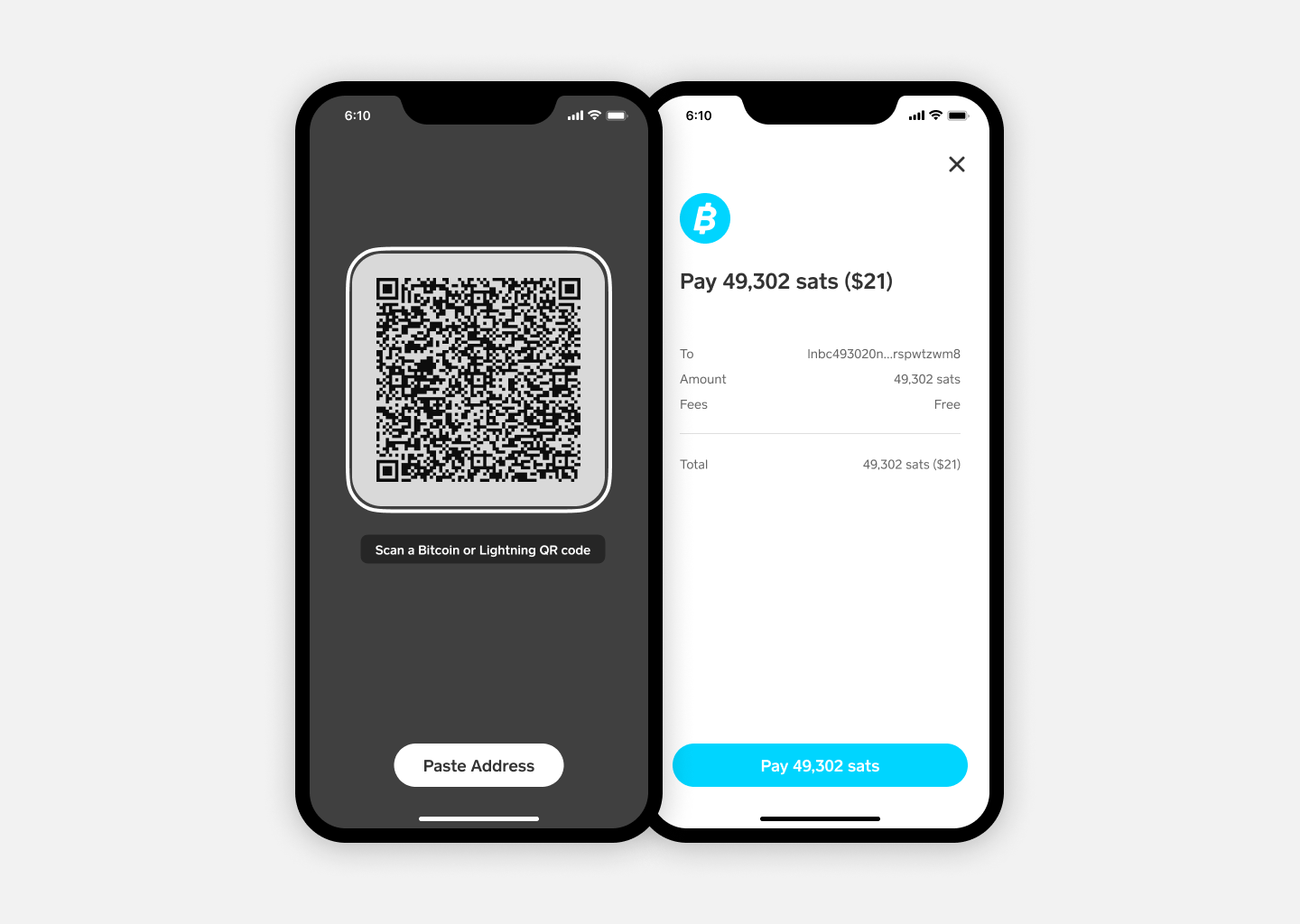

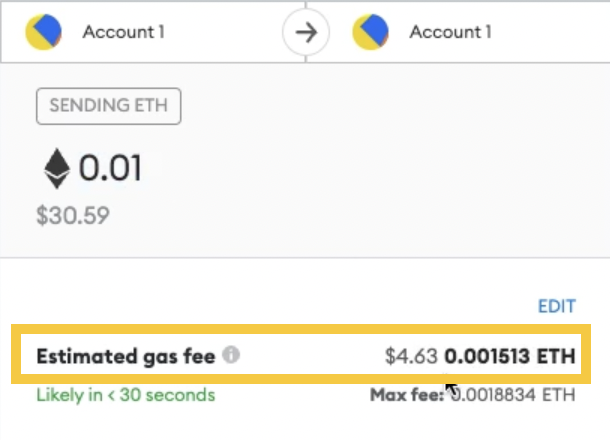

One of the most commonly used features in a Web3 wallet is “Send” – a user flow for, you guessed it, sending crypto from one wallet to another. This user flow contains two new concepts for first-time users: network fees and confirmation delays. Let’s walk through a send flow step-by-step to understand how network fees and confirmation delays impact the UX of Web3. First, users start by copying the address of the wallet they want to send ETH to, and paste it into the first field. They then enter the amount of ETH to send in the bottom field.

The next confirmation screen shows a summary of the transaction, along with the “Estimated gas fee” and a time estimate underneath that (i.e. “Likely in <30 seconds”). This gets back to the network fee and confirmation delay we talked about before. Blockchains are decentralized databases that Web3 modify with their wallets. When someone sends crypto from one wallet to another, we are essentially updating two account balances stored on the blockchain. In other words, the send transaction results in one account being decreased by some amount of ETH, and the second account increased by some amount of ETH.

Remember, the blockchain is a decentralized database. Thousands of nodes store a copy of the blockchain, and must coordinate to update their local blockchains and stay in sync with one another. All this is to say that writing to a blockchain database is much more complex, and expensive, than writing to a centralized database run by one entity. Web3 users pay network fees to these nodes to incentivize them to continue running the blockchain network. I know I just threw a lot at you. Don’t worry if you don’t understand all of this, we’ll talk about blockchains, and how transactions flow through them in later sections.

After pressing “Confirm”, users can go to the “Activity” tab to view the status of the outgoing send transaction. The status starts as “Pending”, and after a bit of time, changes to “Confirmed”. Think back to what I said before – thousands of nodes are coordinating to update the blockchain. This takes time to do. It’s much faster to update VISA’s central database than to update the decentralized blockchain.

Block confirmations, and network fees are the two important takeaways from this section as they directly impact the UX of all Web3 products. Users must pay the nodes that maintain the underlying blockchain in order to use Web3 products, and users also experience a delay in transaction confirmation. Note that blockchains are actively trying to solve UX pain points related to high network fees and long confirmation times. Look into Ethereum Layer 2 scaling and the Solana blockchain to see how UX is moving in the right direction.

Send is one of the main user flows within Web3 wallets, but admittedly not very interesting. There are already many apps out there for sending fiat like PayPal and Venmo. In the next section we will venture all the way into the Web3 ecosystem and connect our wallet to a decentralized application called Uniswap.

1.4 – Connect wallet & access Web3 ecosystem

Decentralized applications, or dApps, are typically web applications that utilize the blockchain as their backend. This is what makes a dApp decentralized. We’ll cover the specifics of dApp software architecture, but for now, we’ll only focus on what the end-user sees when using Uniswap.

Uniswap was one of the first dApps to gain product-market fit in the Web3 ecosystem. It’s a decentralized exchange (i.e. “DEX”) that allows users to swap one token for another. Of course, you can buy and sell tokens on crypto exchanges; however, Uniswap is different in that there are no intermediaries facilitating the trade, or custodying the tokens along the way. Instead, Uniswap, and other decentralized exchanges, run on software deployed to a blockchain that facilitates this token swap in a “trustless” way.

When I say, “trustless” I mean that neither I, nor the strangers I’m swapping with, have to trust each other, or any other centralized entity, to make this swap. All we need to trust in is the objectivity, and deterministic nature of the blockchain. Also, Uniswap’s code is open-source, and can be audited by anyone to ensure that it will execute in the way it’s expected to. “Trustlessness” is a fundamental property of Web3. Let’s walk through swapping tokens on Uniswap.

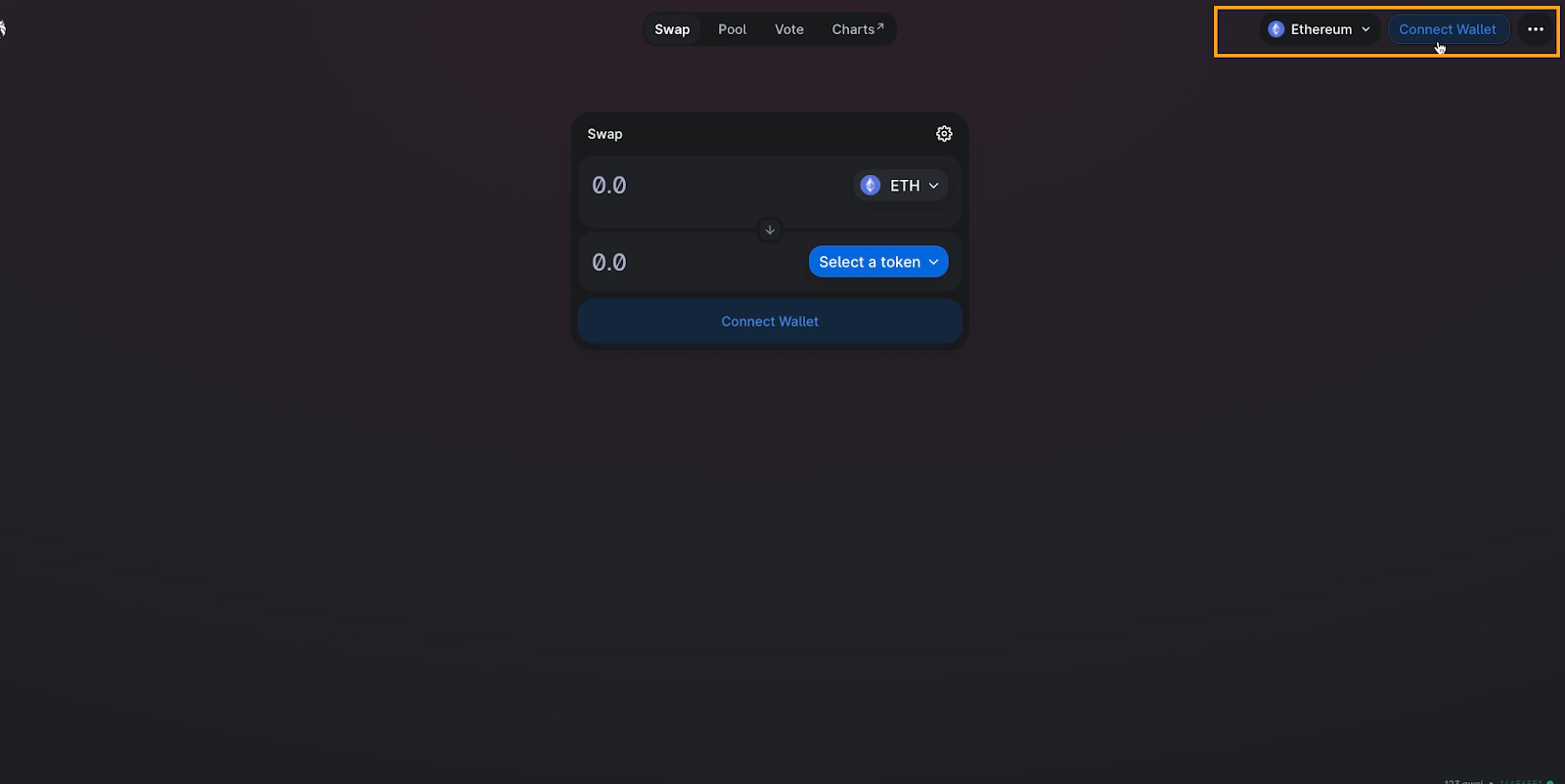

It starts with a fundamental Web3 design pattern: connecting a wallet to the dApp.

A MetaMask popup requires users to confirm this connection request, and allow Uniswap to access their wallet address, account balance, activity, and suggest transactions. Connecting the wallet does not give dApps access to user private keys (i.e. the secret recovery phrase we’ve discussed prior).

Users know the wallet has been connected once their wallet address, and ETH balance, displays in place of the “Connect Wallet” button.

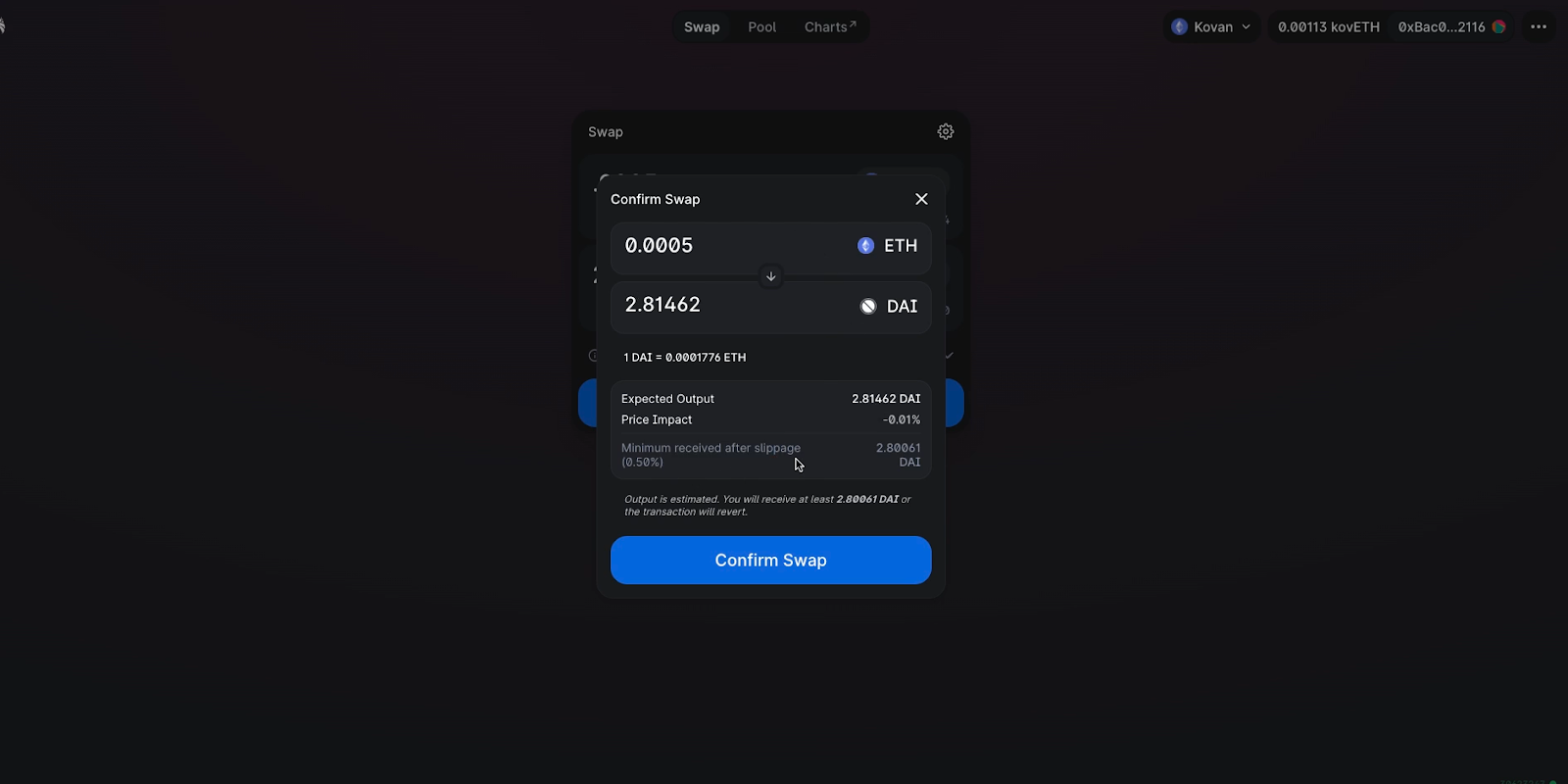

On the Uniswap UI, users select the token they want, and how much of Token A they want to swap.

MetaMask then displays a transaction confirmation screen. This screen should look familiar, because it’s the same confirmation screen that displays during the send flow. Note that the two concepts we talked about in the previous section, network fees and confirmation delays, apply when using Uniswap, and all other dApps for that matter.

Once the Uniswap transaction has been confirmed, users can check that the new token has landed in their wallet.

You may be surprised just how similar this Web3 dApp looks compared to all the Web2 applications that we use on a daily basis. The tech stack used to implement the UI is the same between Web3 and Web2. Both use programming languages like HTML, CSS, and Javascript to build out the frontend UI. The difference comes in when talking about the backend. Web3 backends are built using decentralized blockchains as opposed to the centralized servers of Web2. This is what makes the dApp “decentralized”, and is the source of the unique Web3 properties like “trustless”, “permissionless”, and “censorship-resistant”.

That concludes the user-journey of onboarding into the Web3 ecosystem. We went from fiat money, purchased crypto with it on an exchange, created a Web3 wallet, and transferred the crypto from the exchange into the wallet. We sent crypto to another wallet, and finally connected the wallet to a decentralized application.

1.5 – Web3 wallets and cryptographic keys

You may be wondering where “crypto” comes into play when talking about Web3. Cryptography pervades everything we’ve talked about thus far. It’s the basis for how the average user can self-custody their cryptocurrency, and other digital assets; however, it’s not experienced directly by users. And thank god for that.

We’d be in trouble if users needed an understanding of cryptography in order to use Web3 products. I do think it’s helpful for Web3 product designers to get a base-level understanding of what a Web3 wallet is on a technical-level, and what exactly happens when a Web3 wallet gets created.

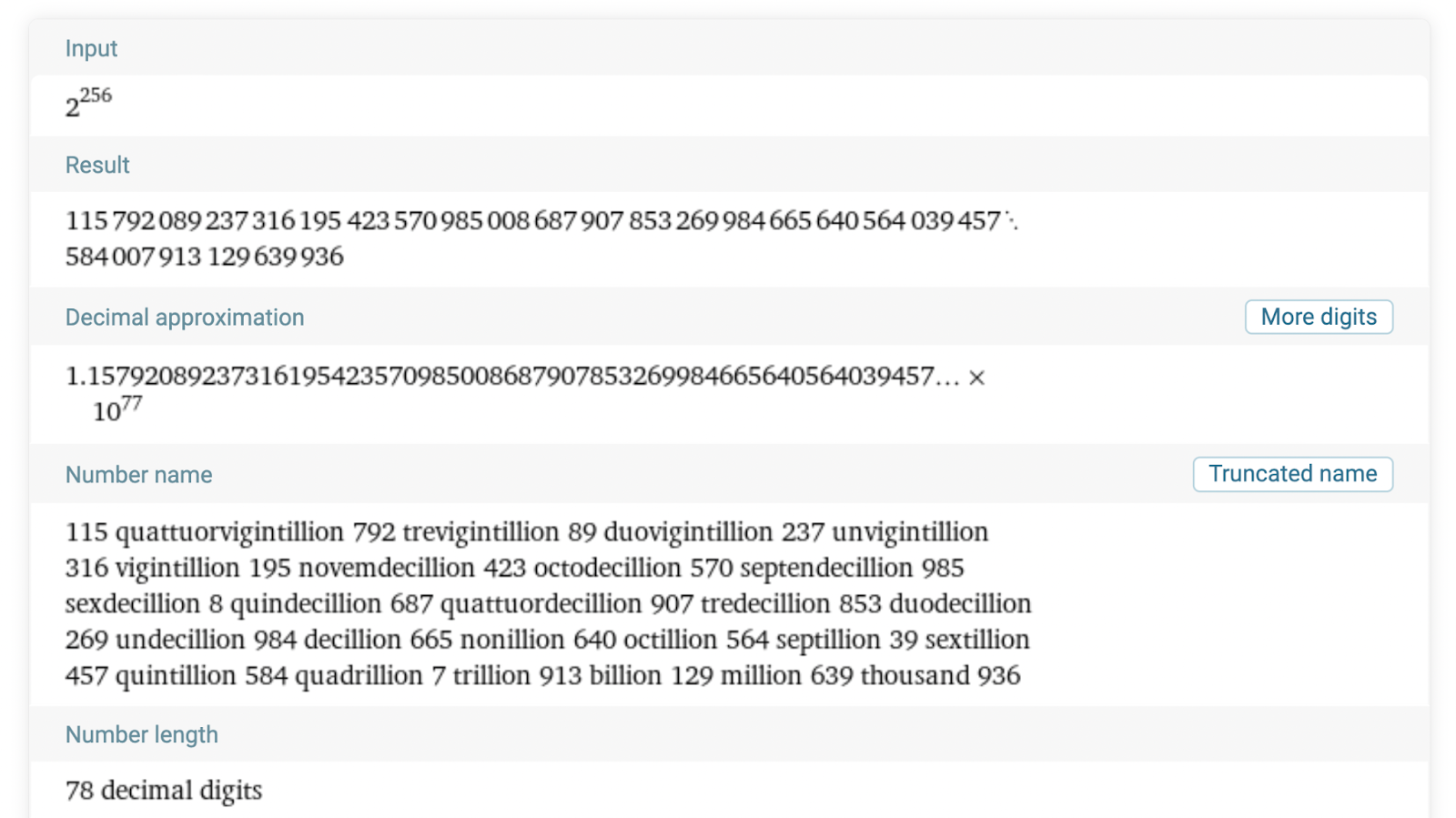

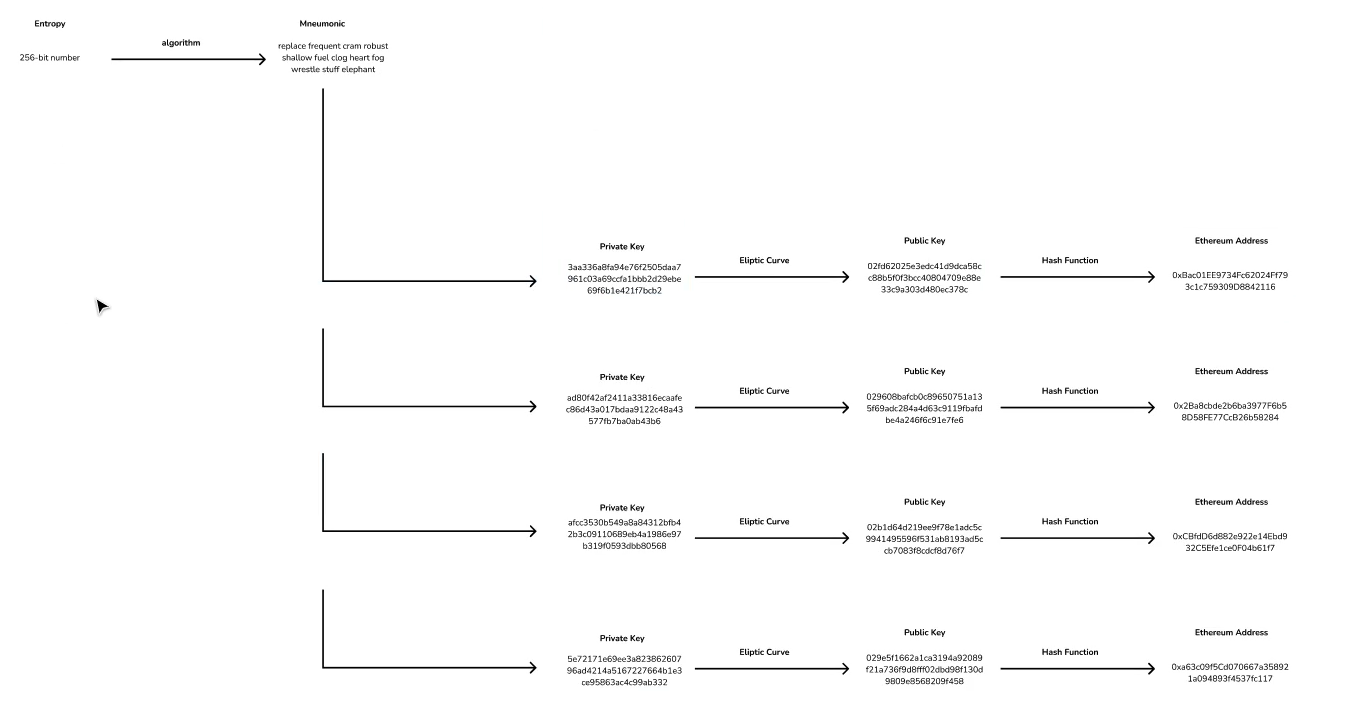

Let’s start off slow, with a concept that is highly counter-intuitive, and will take you weeks to wrap your head around. Not bad for cryptography. To create an Ethereum wallet, you essentially choose a number between 1 and 2^256. The number that you choose is the private key, essentially the password for your Web3 wallet. Let’s talk numbers for a second. 2^256 is a very large number. It’s 78-digits and looks like this…

This is counter-intuitive – that we create our wallet password by randomly picking a number within a set range. Couldn’t someone else randomly guess our wallet’s password by guessing passwords all day? Couldn’t an evil developer code a bot that guesses thousands of private keys per second, checks if the private keys control crypto and, if any do, transfer the crypto to the developer’s wallet? The answer is yes, and yes.

It’s possible for someone to randomly guess your private key and steal your crypto. But the range of private keys is so large (as we just saw above) that it’s practically impossible for anyone guessing in this range to collide with a number that someone else has already guessed. In fact, there are almost as many Ethereum private keys as there are atoms in the Universe (~10^80). The most important thing is that the application creating your wallet randomly selects a number in the range. It’s not advised to choose the number 1, 100, or 1M as a private key.

Now that you understand what a private key is – a random 78-digit number – let’s talk about public keys, and wallet addresses. There is a set process for deriving a public key and address from the private key. Elliptic Curve Cryptography is used to derive the public key from the private key, and the public key is hashed to derive the address from this public key. An explanation of these cryptographic functions is beyond scope, but just understand that the public key, private key, and address are connected to one another. The private-public keys are called “key-pairs”. And this is essentially what an Ethereum wallet is, a private-public key pair. Wallet applications, like MetaMask, manage your key pairs, search the blockchain to see what the balance of your wallet address is, and sign transactions with your private key in order to send crypto, or use dApps.

You may wonder why we’re talking about numeric private keys when, in fact, MetaMask generated a 12-word secret recovery phrase when we created a wallet in the previous section. These 12-words are called mnemonic phrases, and were one of the first major UX improvements in crypto. Rather than making someone write-out a 78-digit number, which could easily be copied incorrectly, users just have to copy a series of 12 everyday words. Wallet apps implement a process for randomly generating this mnemonic phrase, and from the mnemonic phrase, multiple sets of private-public key pairs are derived. This, in itself, is a major UX improvement, because now users can create multiple crypto wallets, each with their own account balances, that can all be recovered using the same secret recovery phrase. You can play around with creating wallets, and seeing how the keys get derived on the backend here.

Okay, so we’ve just learned what happens when you create a Web3 wallet. Wallet apps equip Web3 users with high-grade cryptography that enables them self-custody their digital assets. This is revolutionary, and its importance cannot be understated. Crypto wallets, and blockchain technologies, will fundamentally change how we interact with most software products moving forward.

At this point we understand that the wallet communicates with decentralized applications, and the blockchain, but your understanding of what exactly a blockchain is may still be murky. This is what we’ll tackle in the next section – an explanation of decentralized, peer-to-peer networks.

1.6 – Introduction to decentralized, P2P blockchain networks

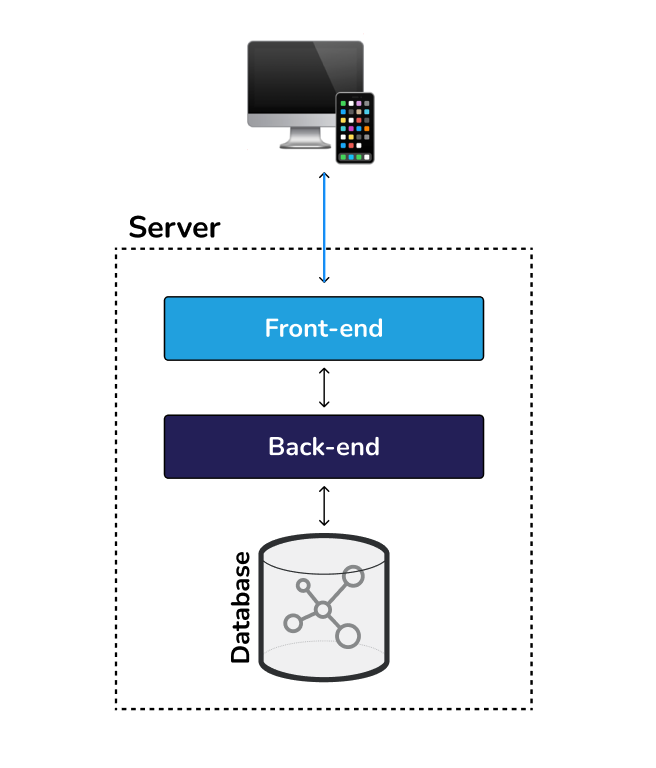

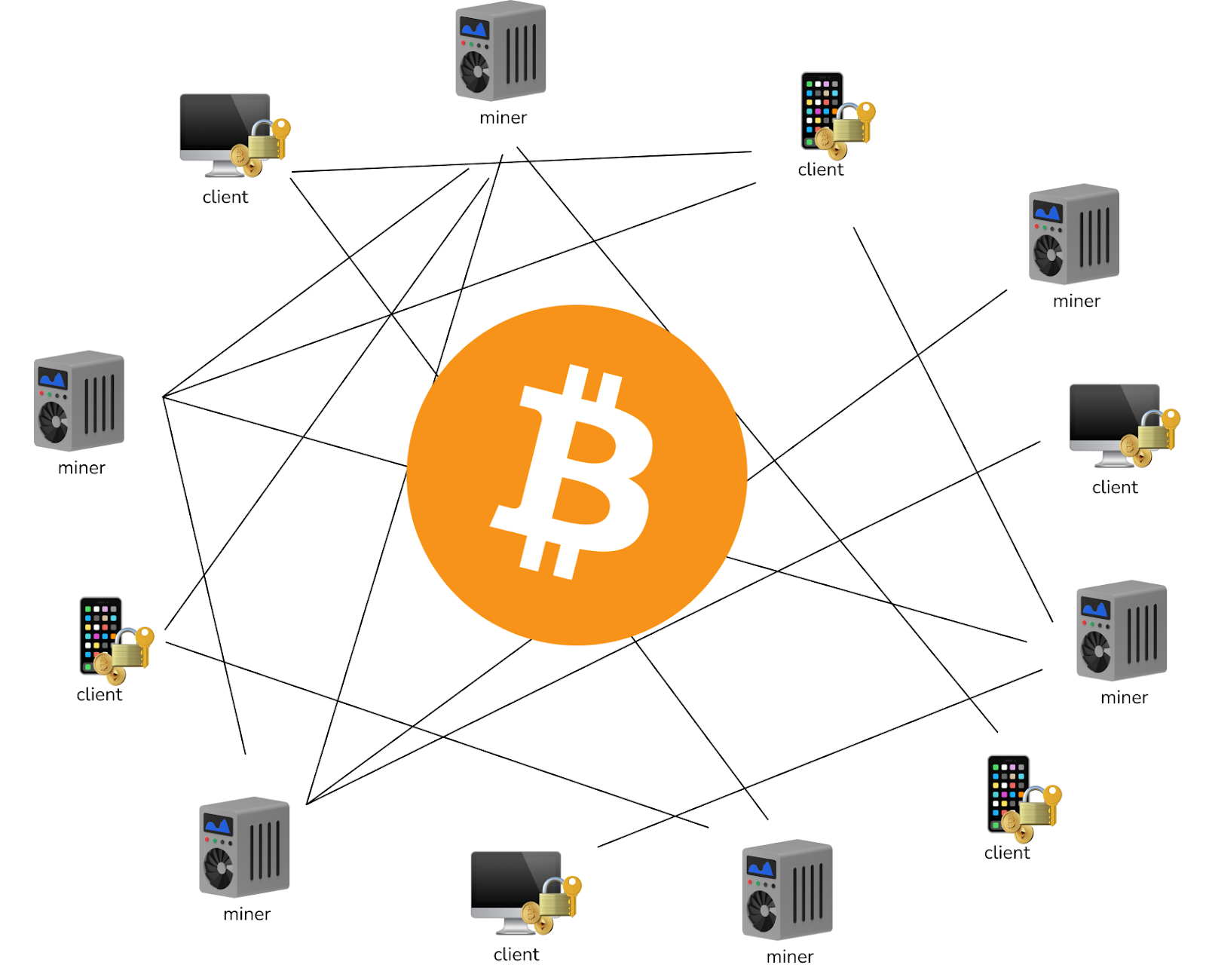

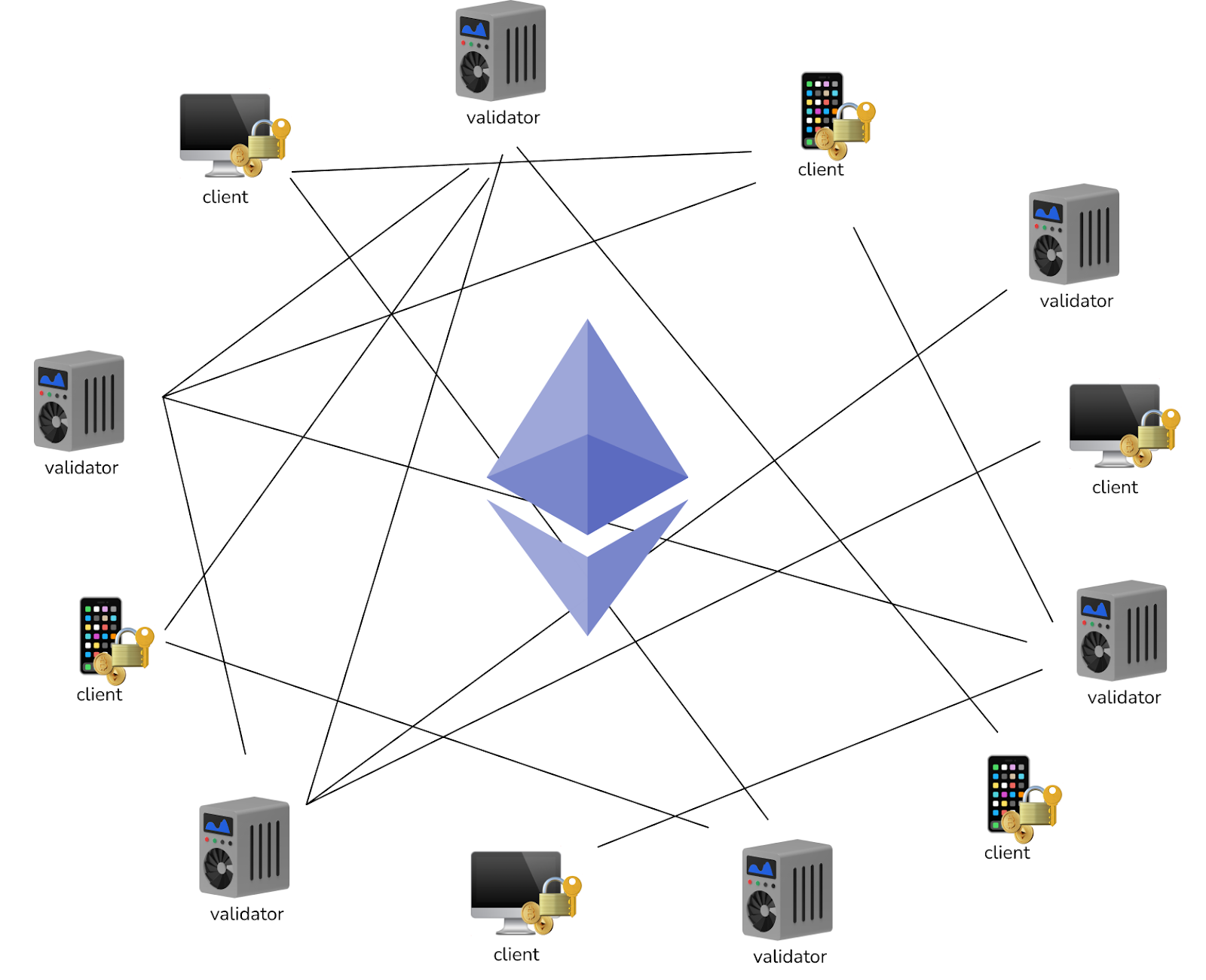

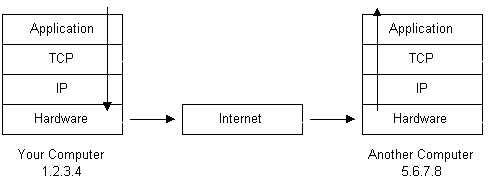

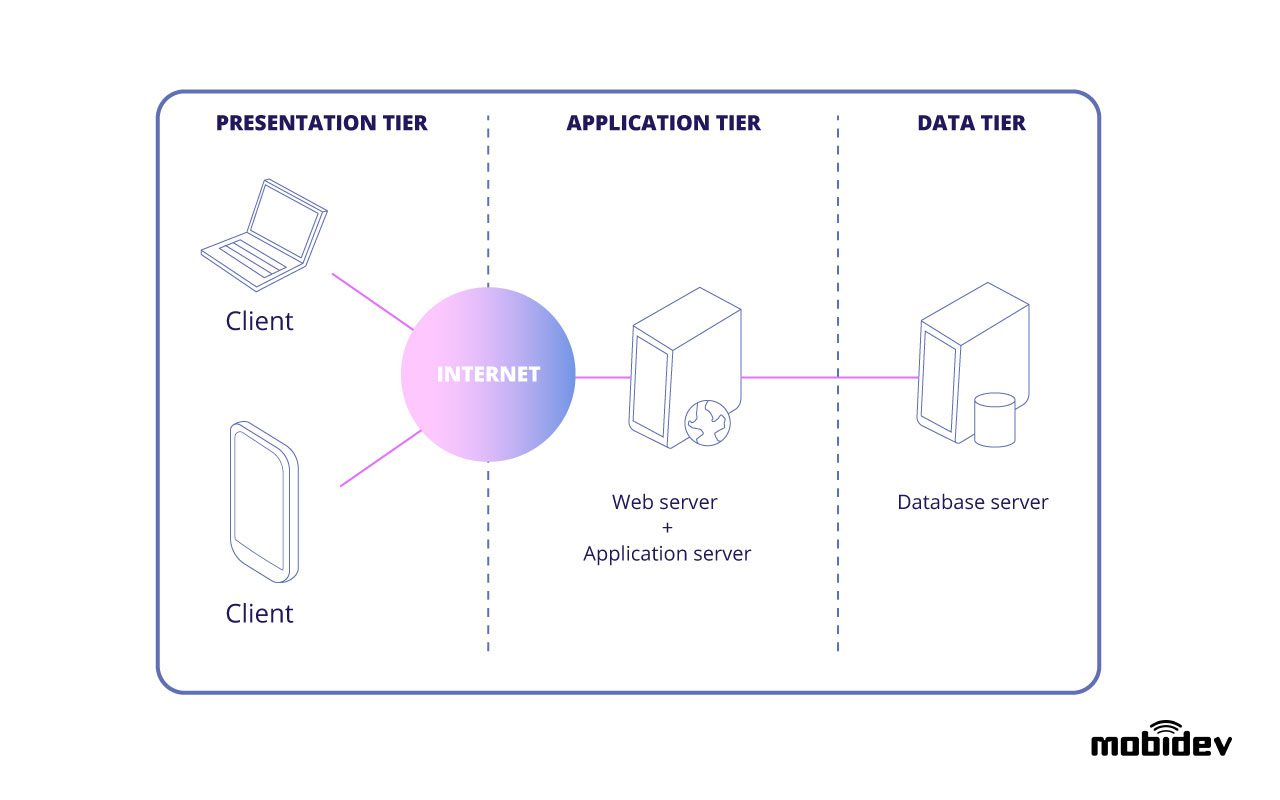

Blockchains are decentralized, peer-to-peer networks. That’s a lot to take in at first, so let’s start with concepts that are familiar to us. Let’s look at how Web2 applications function on the backend.

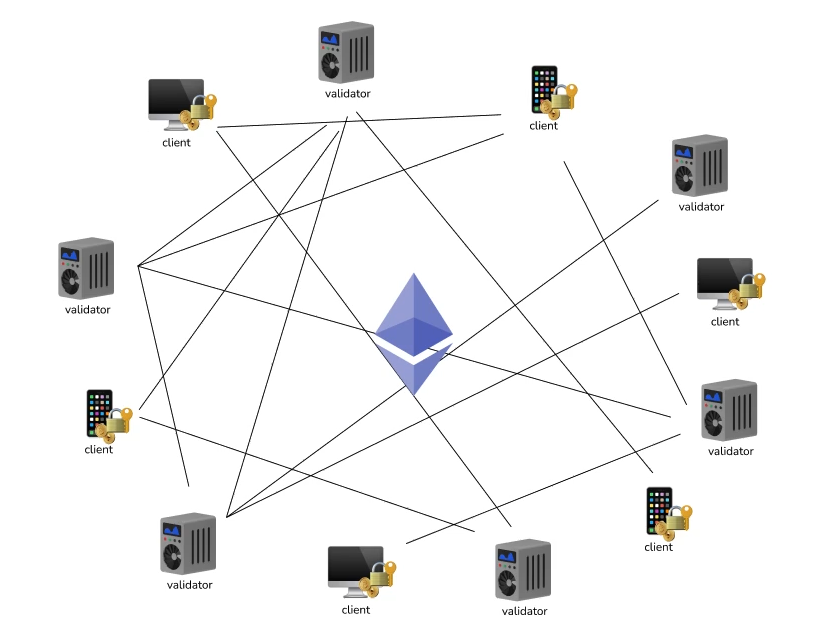

In Web2, computers, smartphones, and tablets talk to servers, and data stores, that are hosted on centralized servers owned by companies like Facebook, Twitter, and Google. These devices, also known as “clients”, use internet protocols like HTTP and TCP/IP to communicate with the centralized servers, and access the web apps. This is what the Web2 internet looks like, and what people have been accustomed to for the past 20 years.

Web3 changes this paradigm. Instead of applications hosted on centralized servers, applications in Web3 are distributed across nodes on a peer-to-peer network. Nodes connect to one another, and no single node “owns” the network, or gets special privileges on the network. In other words, unlike Web2, no single person or company controls access to the network, and has the unilateral right to update the database. Instead, nodes in Web3 must come to consensus with one another, and agree on how to update the blockchain database based on a common rule set. If a node decides to not follow the rule set then it will be unable to participate in the network in the first place.

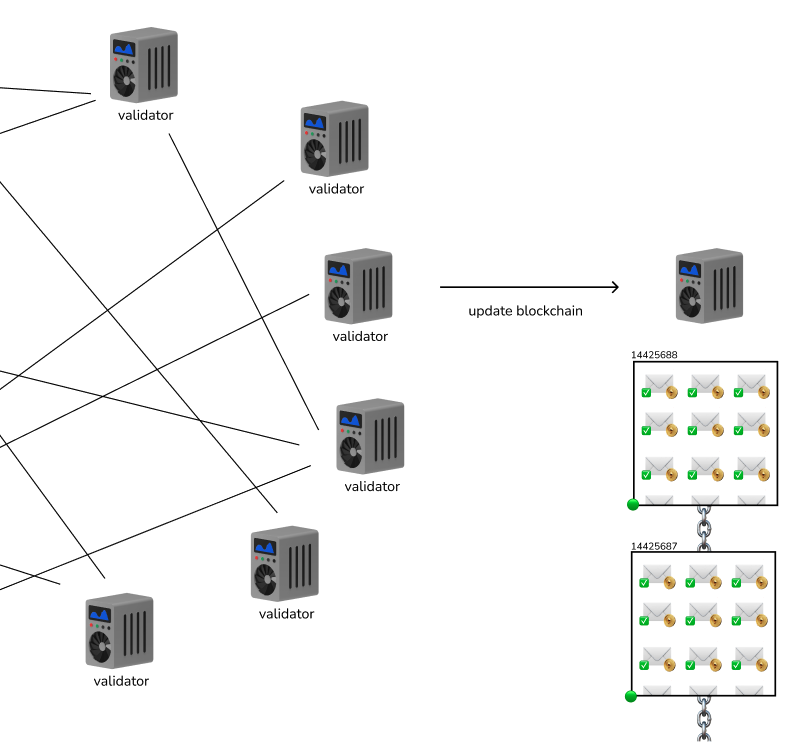

In general, nodes are made up of clients and validators. As we’ve seen in previous sections, Web3 users run wallet software (e.g. MetaMask) on their devices, and send transactions from their wallet in order to transfer crypto, or use dApps. These transactions are sent to, and received by, the validators. Validators are the nodes that do all the work to keep the blockchain running. They all have a local copy of the blockchain, and update the blockchain, by creating new blocks, with the incoming transactions from clients. Remember, no single validator has control over the blockchain, the decision-making is distributed across many validators.

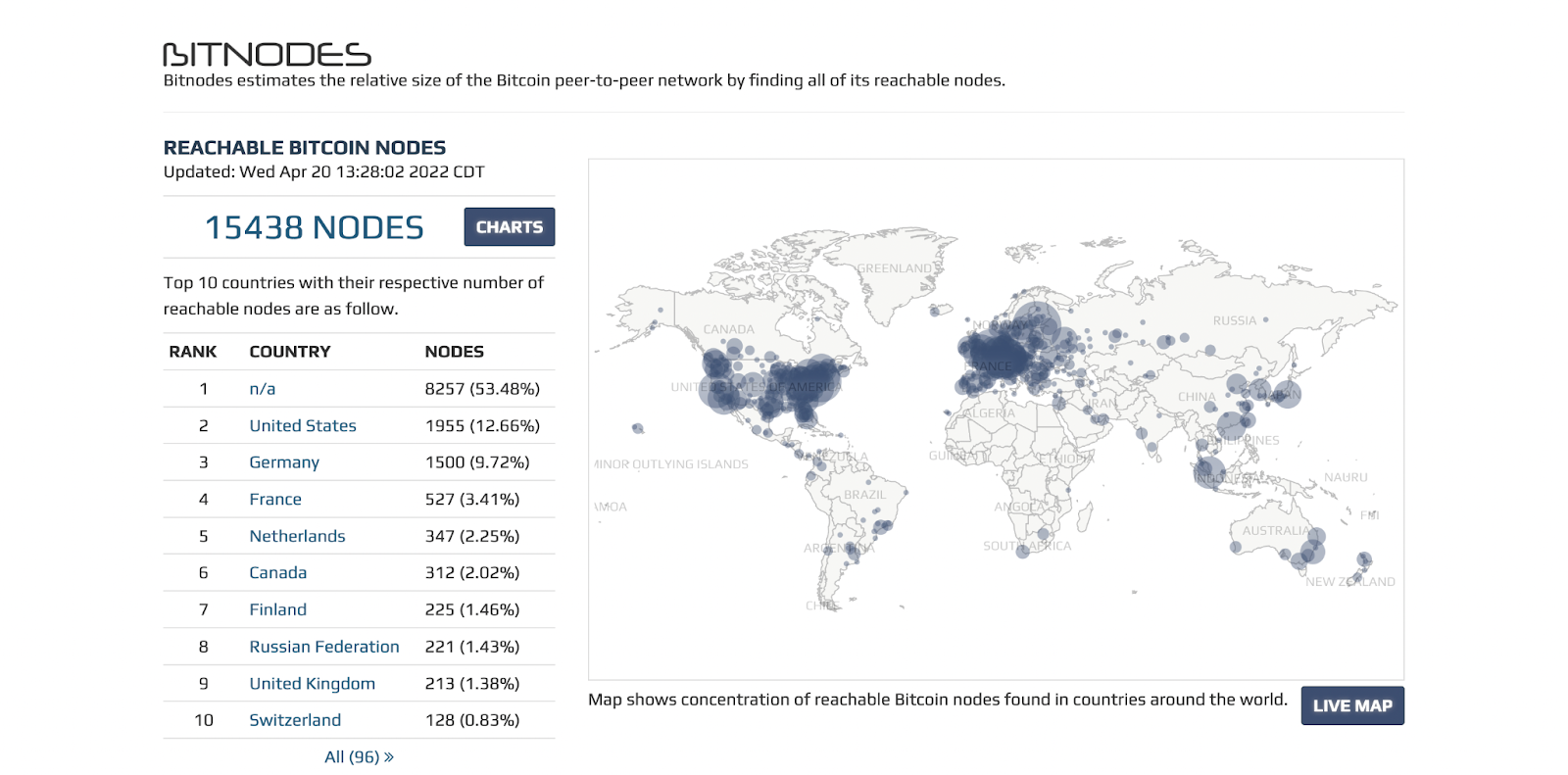

Validators are simply computers running Ethereum node software. In fact, if you wanted to, you could download Ethereum node software to your personal computer, and join the network as a validator. To put it simply, validators do all the work necessary to run the Ethereum blockchain. If you look up real-time stats of Ethereum validators you’ll see that there are thousands of validators on the network, globally distributed across the world. Decentralization results in special properties for the blockchain, and the dApps running on it: resilience and fault-tolerance. Let’s say that the entire UX power grid shut down, and all US nodes went offline. The network would lose 37% of its nodes, but the remaining nodes would continue uninterrupted. This means that the blockchain data (i.e. the history of all transactions) would persist, and decentralized services would continue running.

Now that we know more about what validators are, you may wonder what they actually do to run the network. Essentially, validators are responsible for maintaining the blockchain database locally on their computer. This ensures that the database is distributed and not owned by any single entity. Also, they are responsible for updating the blockchain. In other words, validators create new blocks, adding it to the tip of the current blockchain. Validators propagate new blocks to the rest of the network, so that other validators can check the block, and add it to their local blockchain. Don’t get hung up on the details – this probably won’t make a lot of sense at this point. We’re going to look at this process step by step in the next section. Just understand that validators dedicate their time and resources to maintain the Ethereum network. A reasonable next question might be: why do validators endure these costs to continue running the network?

The incentive is clear, and this is the genius of blockchain networks. Blockchains reward the nodes that run, secure, and support the network with the blockchain’s native coin. On Ethereum, it’s ETH. On Bitcoin, it’s BTC. And so on. As many of you will know, these coins have real monetary value, so there’s financial incentive to not only run the network, but abide by the network’s rule set to ensure maximum return. This token incentive mechanism just described is at the heart of blockchain networks, and decentralized applications. It will be a theme you will continue to see throughout the Web3 ecosystem. We’ll talk more about tokens in later Web3 Design Courses.

In summary, blockchains are made up of a network of distributed nodes that communicate directly with one another. Validators do the work to maintain, and update the blockchain, and they do this to earn rewards paid in that blockchain’s native coin. In the next Section, we’re going to go more in-depth on how the blockchain gets updated, from a client sending a transaction, to a validator including it in a block, to that block getting propagated out to, and accepted by, the rest of validators on the network.

1.7 – Sending transactions to the blockchain

In this section we’re going to talk about what happens on the Ethereum when a crypto wallet sends ETH to another wallet. We’re going to follow this transaction from beginning to end, from the time it’s sent from the crypto wallet, to when it is added to a block, and when the block gets propagated to the rest of the network. This will give us a good idea of the role that nodes play on the blockchain network.

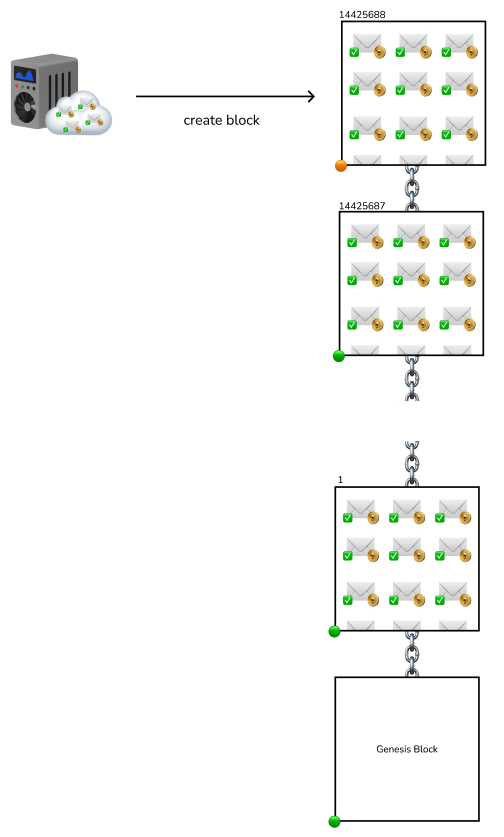

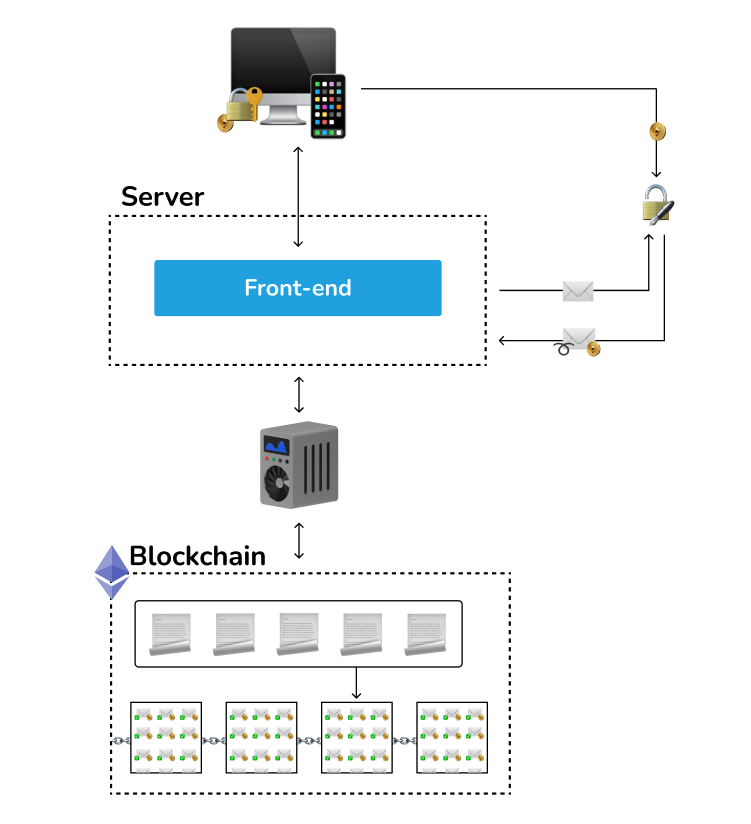

It starts when Web3 users initiate a send transaction from their wallet app. Think of a transaction as a packet of data that contains all the pertinent information, like “from”, “to”, and “amount”. Of course this is an oversimplification, but this has been an adequate mental model of a transaction’s structure for me as a product designer. Next, the wallet signs the transaction with the wallet’s private key. This is called a digital signature and, again, the details are more of a computer science topic than a design topic. The signed transaction is sent to an Ethereum validator who checks that the signature matches the wallet’s public key. Remember from that the private key and public key are intimately related to each other – they are called a key pair. If the signature matches, the transaction is considered valid, and the validator accepts the transaction into its mempool for temporary storage. This process of signing transactions and checking that the signature matches is what secures the user’s crypto, and ensures that only someone with the private key can spend that wallet’s crypto.

Let’s pause for a moment, and talk about blockchains and their constituent blocks. Validators assemble new blocks with the transactions in their mempool. Again, this is an oversimplification, but a block is a larger data packet made up of transactions and some unique information that connects it to the last block. Every block connects back to the previous block, and this goes all the way back to the genesis block. The genesis block is the first block on the blockchain, and initiated the Ethereum blockchain on June 30th, 2015. Since then, the blockchain has been built up, block by block. So the blockchain is simply a record of all the confirmed transactions from the genesis block onward. A validator creates a new block, roughly every 12 seconds on Ethereum, with the confirmed transactions that have been received since the last block.

Now that a validator has created a new block, the validator sends the block out to the rest of the network. This is called block propagation, and goes back to the fact that the network is decentralized, and no single validator has the authority to update the blockchain. The validator essentially proposes the new block to other validators, who check that the new block meets certain criteria, and if it does, the other validators add it to their local blockchain. This is how the blockchain gets updated.

When all the validators have the same blockchain, updated with the newest block, then the transactions within the newest block go from pending to confirmed. Thus, Web3 users must wait for their transactions to be included in a block, which has to do with the block confirmation delay we discussed in section X.

Also, remember how Web3 users must pay a network fee with every transaction they send. And blocks are made up of these transactions. Every time a new block is created, the network fees get distributed to the validators participating in the network at that time.

To bring this back to our original example of sending crypto to a friend, my send transaction was included in a block, and the validators added the block to their blockchain. This is when my transaction went from pending to confirmed. My wallet’s account balance was decreased by X + F ether, my friend’s account balance was increased by X ether, and F ether was distributed to the validators.

Last thing to discuss – Ethereum is a public blockchain meaning that the data is open for anyone to see. There are tools called block explorers that are great for looking at the status of the network in terms of what was the most recent block, when it was created, and by which validator. Also, you can see all the transactions that were included in a block. Further, you can look into transactions and see the wallet address from which it originated, which address it was sent to, and the amount that was sent.

In summary, we looked at what happens behind the scenes when one wallet sends ETH to another. And we now understand the roles of each node on the Ethereum network. Clients running crypto wallet software are responsible for assembling raw transactions, signing raw transactions with the wallet’s private key to legitimize them, and sending these signed transactions to validators on the blockchain. Also, the wallet software queries the blockchain to get the status of the transaction, whether it’s pending, or if it’s been confirmed. Also, the wallet app queries the wallet’s address to return information like token balance, which then gets displayed on the UI for the user to see.

Finally, validators are responsible for receiving incoming transactions, and checking their legitimacy. They create new blocks to update the current state of the blockchain by bundling these confirmed transactions, and send the new block on to other validators so that it propagates across the network. The other validators check that the block is valid, and then accept it and add it to their blockchain. This is how the blockchain gets updated, and all validators end with the same copy of the blockchain, stored locally on their computers.

1.8 – Interacting with dApps on the blockchain

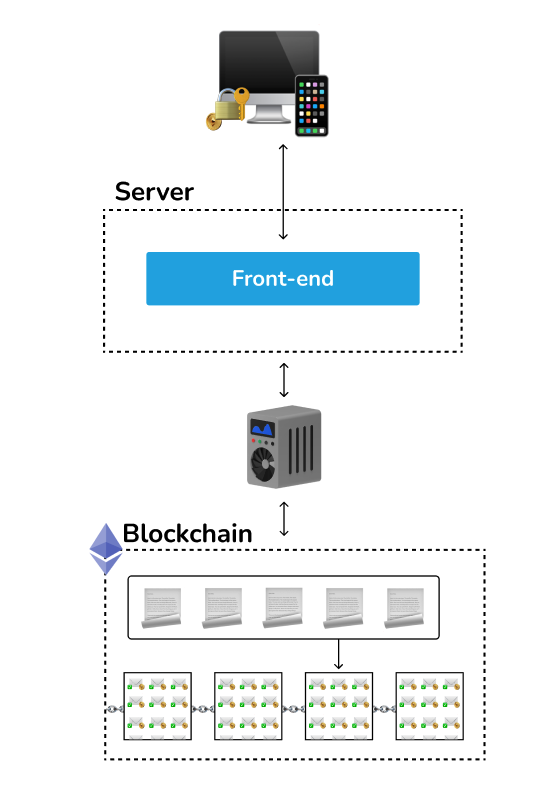

Now that we’ve learned what a blockchain is, and understand how transactions flow through the network, let’s return back to decentralized applications, or dApps. We already looked at Uniswap, a dApp that facilitates token swaps. In this section, we will break down what exactly a dApp is. We’ll start by quickly reviewing the software architecture of Web2 applications then compare it to that of Web3 dApps.

Web2 applications are hosted on a company’s centralized server. At a high level, the web app has a frontend, backend and database associated with it. A user’s computer communicates with the company’s server using internet protocols, and frontend code (e.g. HTML, CSS, and Javascript) is sent to the user’s computer where it is then rendered into a UI within an internet browser. Because of this centralized software architecture, the company has unilateral rights to update the application’s code and modify its database. And for good reason as this is how new versions of web apps get deployed to user communities; however, companies can do a number of things like censor user content, and even outright ban users from their web apps. What’s more, Web2 companies often monetize user content and data via advertising. In other words, the companies earn massive profits while the users who generate content, and make up the site traffic, capture little of the value they create. This is counterintuitive, but has become normalized as it’s been the dominant internet business model over the past 20 years. We’ve never known of anything different until now.

Web3 disrupts this paradigm with decentralization. Like Web2, frontend code is still rendered into a UI with internet browsers, but the dApp’s backend is where things start to differ. Instead of a centralized server, Web3 dApps deploy backend code to the blockchain with smart contracts, and also utilize the blockchain as a decentralized database. No company owns the dApp, or the blockchain that the dApp leverages. As we saw before, dApps are permissionless so anyone can use them, and the blockchain database can only be updated by a user with their private key.

Now think back to our example of swapping tokens on Uniswap. We connected our wallet to Uniswap, and initiated the swap from ETH to DAI on Uniswap’s UI. On the backend, Uniswap assembles the raw transaction necessary to make this swap. We can imagine the raw transaction contains data like wallet address, how much Ether I want to swap, and how much DAI I expect in return. The transaction also points to the swap function within one of Uniswap’s smart contracts, which is stored on the Ethereum blockchain. But more on this later. We learned from the previous section that the validators will not accept unsigned transactions; therefore, Uniswap sends the raw transaction to a user’s wallet, the wallet app signs the transaction (after the user accepts a MetaMask confirmation popup) with the private key, the signed transaction is sent back to Uniswap, and Uniswap sends the signed transaction to an Ethereum validator.

Now we’re back to what we discussed in the previous section about what happens once a transaction has been sent to an Ethereum node. A validator checks the validity of the signed transaction, includes it in a new block, propagates the new block through the network, and so on. Once this block gets accepted by the other validators then the user’s Uniswap transaction goes from pending to confirmed, his/her account’s ETH balance is decreased by X plus a network fee, and increased by Y DAI. The swap is complete.

Remember dApps deploy their backend code to the blockchain in the form of smart contracts. One of the main features of Uniswap is, of course, its swap functionality, so, somewhere, in one of its smart contracts, we’d expect a swap function. When smart contracts get deployed to the blockchain, a contract address is created that looks identical to a Web3 wallet address. This is where the smart contract code lives. Once a smart contract has been deployed to the blockchain it cannot be modified or deleted – it is “immutable”. The smart contract is also permissionless in that anyone can use it, like a public utility. Also, anyone can audit the code, line by line, to ensure that it will execute in an expected manner.

You can think of smart contracts like a vending machine. You put money into a vending machine along with which snack you want, and the vending machine outputs the snack. As we saw before dApps assemble raw transactions that point to smart contract addresses, and the functions within them, to carry out whatever the user requested. ETH is also attached to this transaction to pay the validators for processing the transaction. The transaction passes in parameters to the swap function like wallet address, amount Token A, amount Token B. Finally, the smart contract updates the state of the blockchain accordingly (i.e. user’s ETH and DAI token balance).

2 – Evolution of Blockchain Ecosystems

Blockchains enable Web3. Without blockchains, we wouldn’t have crypto tokens and most of the decentralized applications that are running today. This chapter will give Web3 product designers an understanding of where blockchains came from, what the current blockchain landscape looks like, and where blockchains are headed in the future.

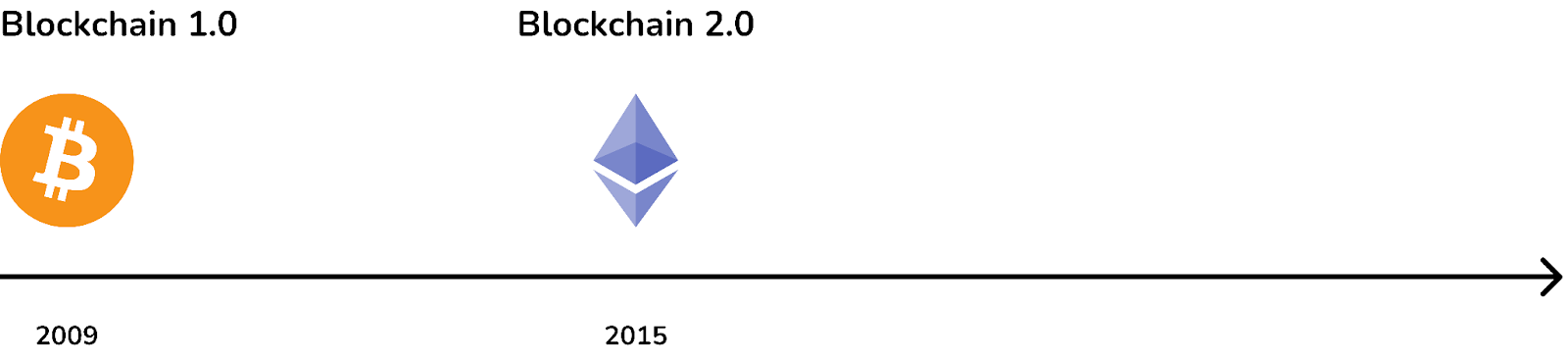

Bitcoin was created by an anonymous figure, named Satoshi Nakamoto, and released as open source software in 2009. Looking at the Bitcoin Whitepaper, Satoshi intended Bitcoin to be a digital currency that could be exchanged without any intermediaries like banks. Bitcoin is simple compared to later blockchains. It’s essentially a ledger that tracks the transfer of bitcoin cryptocurrency between wallet addresses. This ledger is decentralized in that it is distributed across thousands of nodes worldwide. Now, 13 years later, Bitcoin has a market capitalization hovering around $1 trillion.

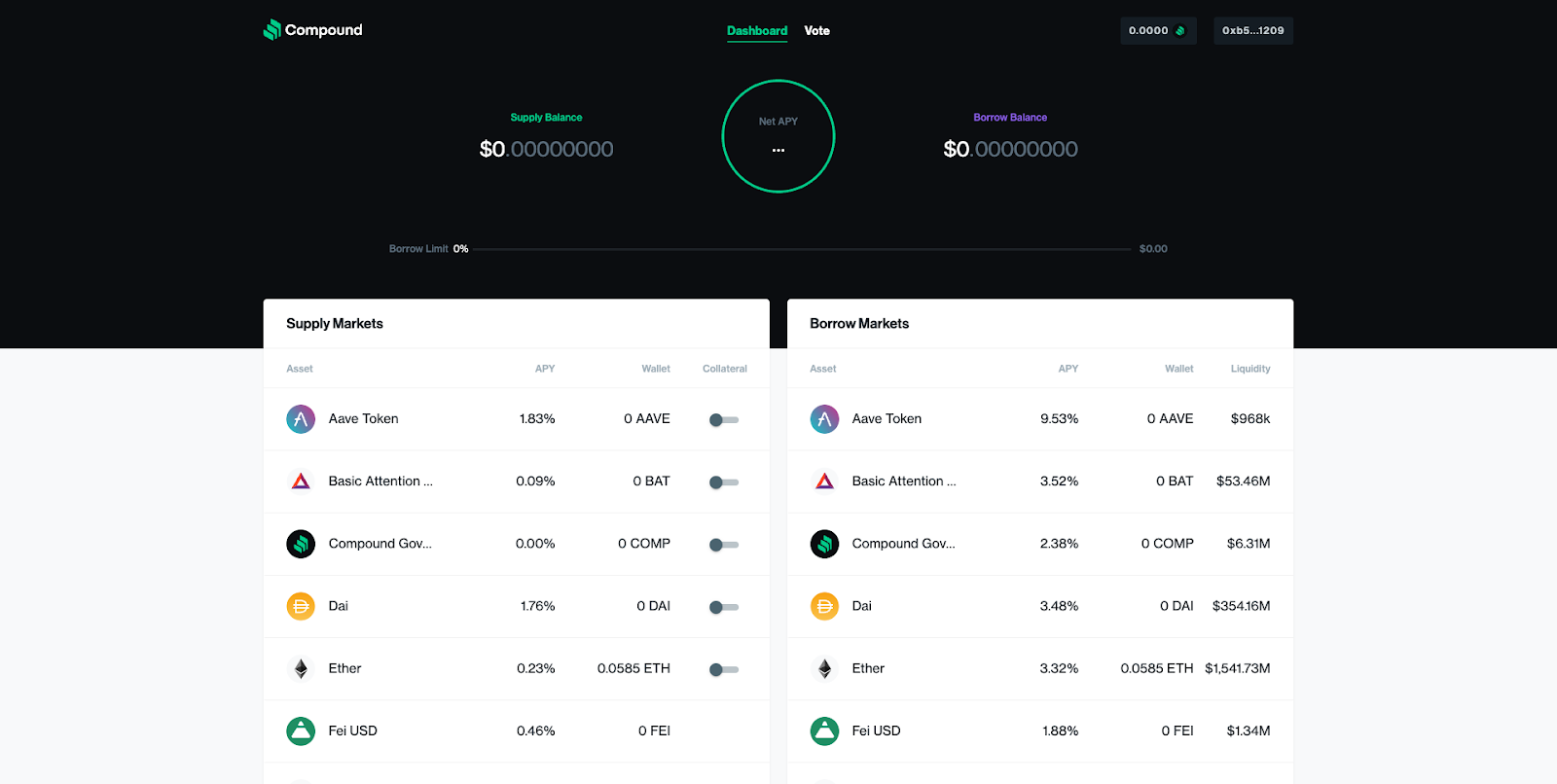

Ethereum, initiated in 2015, was the next phase in blockchain development. The fundamental innovation of Ethereum is that it generalized blockchains from a simple currency ledger to a virtual machine that can run decentralized applications. Thousands of third-party developers have built up an ecosystem of dApps on Ethereum ranging from decentralized finance (e.g. Compound & Uniswap) to NFT trading platforms (e.g. OpenSea & SuperRare). These new use-cases onboarded millions of users to Web3, which brings us to the present day.

With this increase in demand, Ethereum is now maxed out in terms of processing user transactions. Thus, network fees have skyrocketed. Some transactions can cost over $100, which has made using Ethereum prohibitively expensive for the average user. Ethereum has plans to scale with its transition to Ethereum 2.0; however, other smart contract blockchains with novel design philosophies and software architectures are currently emerging. Indeed, the blockchain landscape is developing rapidly, and each Layer 1 blockchain has its own Web3 ecosystem growing on top of it. Some honorable mentions include Polkadot, Solana, Cosmos, Algorand, Luna, Avalanche, and more.

2.1 – Bitcoin, the World’s First Blockchain

In the introduction, we talked about how Bitcoin was the first blockchain ever, and it powers a peer-to-peer digital currency that can be exchanged without intermediaries like banks, or payment processors. But this is all sort of abstract. What is Bitcoin exactly?

There are several layers to Bitcoin – let’s talk about each. First, Bitcoin is a piece of open-source software that is referred to as the Bitcoin Protocol. Open-source means that anyone can download it, and any developer can suggest improvements to the protocol or build applications on top of it. Satoshi released the first implementation of the Bitcoin Protocol, called Bitcoin Core on Github in 2009.

When someone installs, and runs, Bitcoin Core their computer becomes a node on the Bitcoin network, which brings us to the second layer. Bitcoin is a decentralized, peer-to-peer network of Bitcoin nodes, or computers running the Bitcoin Protocol. The protocol defines the rule set for how these nodes interact with one another in order to keep Bitcoin up and running.

For example, when I first run Bitcoin Core, my computer connects to other Bitcoin nodes and downloads the Bitcoin blockchain from them, which is a file of around 400GB. This brings us to the third, and final, layer of Bitcoin. Bitcoin is a blockchain that tracks the movement of a decentralized digital cryptocurrency called bitcoin (BTC).

Remember the blockchain is simply a ledger that is distributed across all the Bitcoin nodes. In other words, each Bitcoin node stores its own copy of the Bitcoin blockchain – this is what makes blockchains decentralized. But how does the blockchain get updated in a decentralized way? If one Bitcoin node had unilateral rights to update the blockchain with new transactions then this would defeat the purpose of decentralization. Nodes take turns updating the blockchain, and coordinate with each other based on a predefined rule set specified in the Bitcoin Protocol.

When a node creates a new block, and adds it to the blockchain, and the other nodes accept the new block, and add it to their blockchains – this is called “consensus”. Bitcoin uses something called “Proof of Work” as its consensus mechanism. This is a highly technical topic, so just understand that, with Proof of Work, nodes must spend large amounts of electricity and computing resources to win the right to create a block and update the blockchain. This high energy expenditure is by design, and is what prevents the blockchain from attackers; however, it’s also a criticism of Bitcoin. The Bitcoin Network consumes a comparable amount of power to Thailand, which critics argue is bad for the environment.

Consensus mechanisms are important when it comes to the technical design of blockchains. They have a great impact on the security and performance of blockchains. We’ll see in later sections the innovations that are taking place around consensus mechanisms within emerging blockchains.

Bitcoin Protocol is open-source software that establishes the Bitcoin node network, which maintains the Bitcoin blockchain, which tracks the movement of bitcoin cryptocurrency. I know this is confusing – bitcoin (lower-case “b”) is the native cryptocurrency of the Bitcoin protocol (upper-case “B”). Nodes are rewarded with bitcoin when they create a block – this is what incentivizes them to spend electricity to win the right to do so. This reward is also called “bitcoin issuance”.

You may wonder how a digital currency can be valuable. Most of the digital content we’re used to, like images, can be replicated millions of times for free. This brings us to the concept of “tokenomics”, or token economics, which has to do with the monetary policy of cryptocurrencies. A limit on the total bitcoin that will ever be issued is encoded directly in the Bitcoin protocol. Once 21M bitcoin have been issued, estimated to happen sometime in the year 2140, then no more bitcoin will be issued. This limit of 21M is called a “hard cap”, and is the most important thing to understand about bitcoin’s monetary policy. It’s fundamental to why people believe bitcoin has real value.

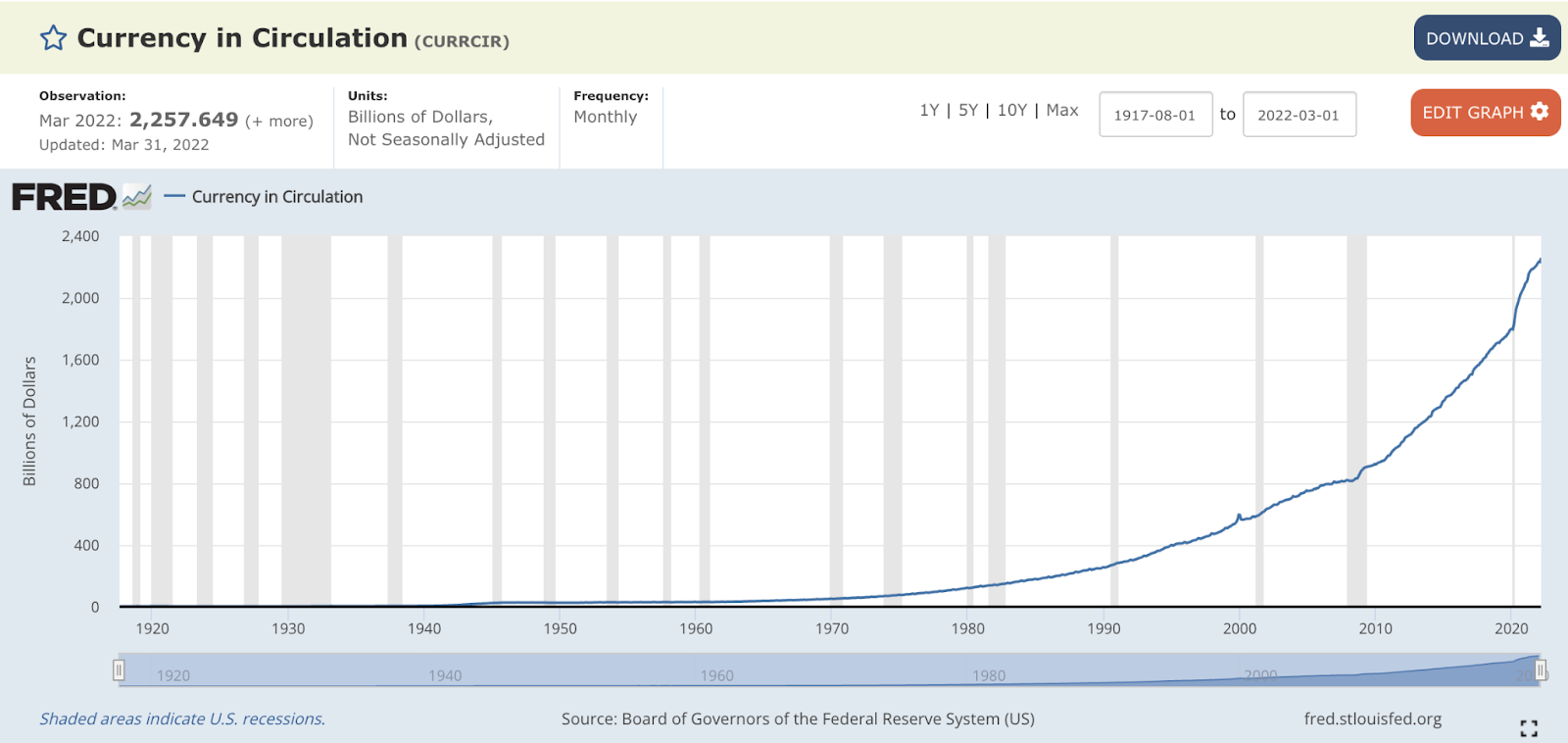

Juxtapose this 21M bitcoin hard cap to the US dollar. $3.38 trillion were issued just in the year 2020, largely in response to the COVID outbreak. This increased the supply of US dollars by about 20%. There is no hard cap to the US dollar. The Federal Reserve (FED) has total control over the national currency, and can issue as much currency as they see fit. When you create more of something it becomes less scarce and, assuming constant demand, less valuable. This is why you may have heard people say that the currencies are being devalued.

So how can bitcoin, a digital currency currently trading at ~$40,000, demand this real world value? There is a fixed supply of bitcoin, so if demand increases then the price of bitcoin will increase. And there is always demand to own assets that hold value or, better yet, increase in value over time. Bitcoin hasn’t seen a great amount of adoption in terms of a currency – something that people use to pay for goods and services (although this could change with the mainstream rollout of Bitcoin’s lightning network). Instead, bitcoin has seen adoption from retail investors, and increasingly institutions, under the premise of “bitcoin as a store of value”.

Scarce resources have been the backbone of currencies for thousands of years. Gold is a good example. One of the reasons it’s valuable is because it’s naturally scarce and difficult to extract from the Earth. Gold is the original store of value asset; however, there’s still a problem with gold. The global supply of gold is estimated to increase by around 2% per year.

Michael Saylor, a prominent Bitcoin evangelist, talks about how bitcoin is the only solution for transferring your money over 100 years – everything else loses its value entirely due to asset inflation. Let’s follow his line of reasoning. He estimates fiat currency (like the USD) is currently inflating at 15% per year, which means you lose all the purchasing power of your money in less than 5 years. Going back to gold with its 2% annual inflation – you lose all your purchasing power in 36 years. Saylor reasons through other assets like real-estate, but it’ll be much more entertaining to hear it from him. Gotta love his delivery.

So now you can start to see why bitcoin is thought of as a store of value by an increasing number of investors. The Bitcoin community seems to be content with this limited use-case as evidenced by slow and conservative upgrades to the Bitcoin protocol. Interestingly, bitcoin has not seen much adoption as a currency to pay for everyday goods and services, but this could change soon with the rollout of Bitcoin’s lightning network in mainstream products like Cash App.

That’s Bitcoin in a nutshell. We talked about how Bitcoin is open-source software, a network of nodes, and a blockchain ledger that tracks the bitcoin cryptocurrency. Also, the 21M hard cap grants bitcoin the never-before-seen property of digital scarcity. An increasing number of investors consider bitcoin a store of value asset, similar to gold. The next section covers the second evolutionary phase of blockchains, which enables the growth of a Web3 ecosystem of dApps.

2.2 – Ethereum & the Advent of Smart Contract Blockchains

Ethereum, launched in 2015, marks the second evolutionary phase of blockchains. Vitalik Buterin, the founder of Ethereum, was an early-adopter of Bitcoin, but saw the potential for blockchains to power additional use-cases beyond just decentralized digital currencies. Let’s compare Bitcoin and Ethereum by way of analogy.

If Bitcoin is like the calculator app on a smartphone then Ethereum is like a smartphone in itself. Bitcoin is designed to serve one, specific purpose. Ethereum, on the other hand, can run any number of applications. Third-party developers deploy applications to Ethereum like they do with the Apple App Store on the iPhone.

Bitcoin and Ethereum are actually similar in many regards. Both are open-source software, anyone can become a node on the network, and nodes are responsible for accepting transactions and creating blocks; however, Ethereum has an extra layer of complexity built into it, allowing developers to deploy decentralized applications via smart contracts.

Bitcoin is a more conservative blockchain protocol than Ethereum with regards to protocol upgrades. Ethereum has an aggressive roadmap for improving its protocol as we’ll discuss later on. The development ethos of Ethereum is to move fast and break things – and explore what is possible when it comes to building Web3 ecosystems.

Ethereum was the first smart contract blockchain, and is the most dominant smart contract blockchain to date, coming in as the second most valuable cryptocurrency behind Bitcoin. Just as Bitcoin’s native crypto is bitcoin, Ethereum’s is ether; however, ether has a utility aspect to it that bitcoin does not.

Ethereum is general purpose in that it will run any smart contract code that developers deploy to the blockchain. The problem with general purpose coding is that programs are not guaranteed to reach an end state – they can continue to loop forever. This is a problem because looping programs would tie up Ethereum nodes indefinitely, disallowing them from processing other incoming transactions. Thus, an incompetent, or malicious developer could write a program that halts Ethereum. This is referred to as denial of service (DDOS) and is one attack vector that blockchains need to defend against.

Ethereum solves this problem by making users pay for the amount of computation their transaction consumes. To send ether from one address to another is a simple transaction, and requires relatively little computation. Still, users pay nodes to process this transaction with a network fee, let’s say around $5. Now, when someone uses a dApp, which might call multiple smart contracts on the backend, this added computation is accounted for with a higher network fee (e.g. $20). Thus, it gets prohibitively expensive to tie up the Ethereum blockchain for any significant amount of time.

Ether is a digital currency as well. You can send ether between wallets, and Ethereum wallets have ether balances, just like Bitcoin wallets have bitcoin balances. But ether has added utility over bitcoin in that it powers decentralized applications. This is why ether has a different investment narrative than bitcoin’s store-of-value narrative. Ethereum is a platform similar to an app store. Ethereum’s value as a platform increases as developers continue to deploy useful dApps to it, and Web3 users access these decentralized services by paying ether. Ether as a cryptocurrency has a totally different tokenomics to that of bitcoin, but that’s out of scope for now.

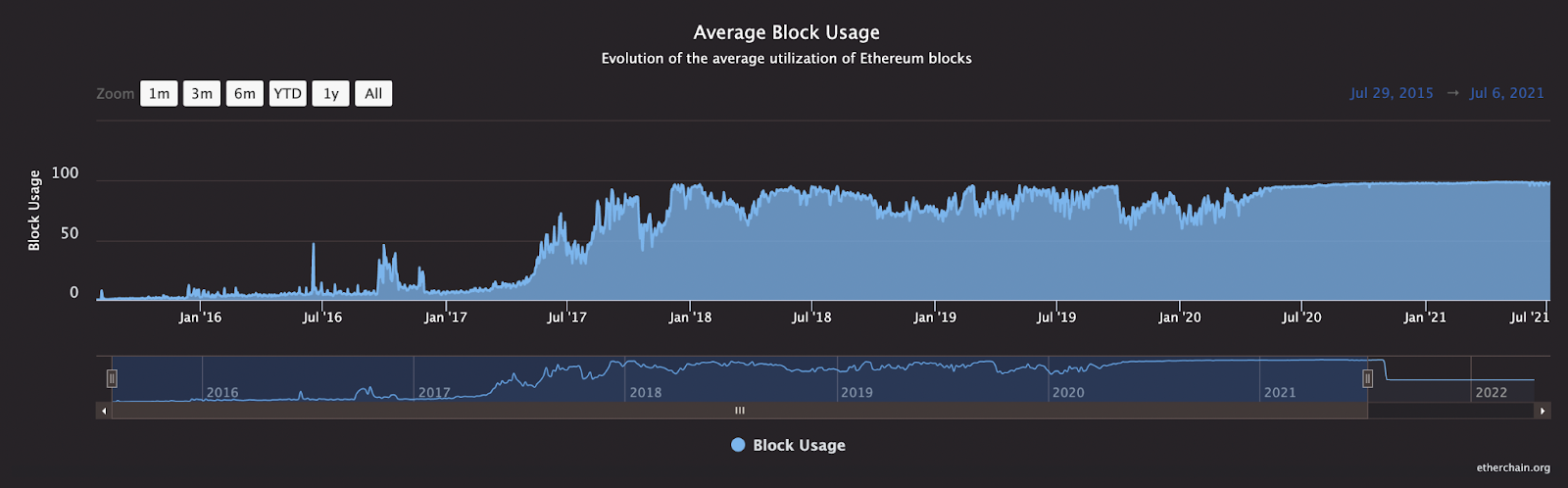

Let’s return to the idea of network fees. Ethereum nodes create new blocks roughly every 12 to 14 seconds, and only a certain number of transactions can be included in each block. This means there is a limit to the number of transactions per second (TPS) that Ethereum can process. In fact, Ethereum can handle roughly 30 TPS. With demand for dApps increasing, demand for Ethereum’s finite blockspace increases, thus driving up network fees.

This especially became a problem with a recent wave of DeFi and NFT-related traffic to Ethereum. The average network fee was as high as $49 per transaction at one point in 2021. Personally, I saw several hundred dollar network fees when using dApps like Uniswap and Aave. And since I was transacting with relatively small amounts of crypto, these high network fees made the transaction not worth submitting. Layer 1 Ethereum has become prohibitively expensive for the average user. In other words, Ethereum needs to somehow process more transactions per second if it wants to retain current users, and onboard the next 100M users to Web3.

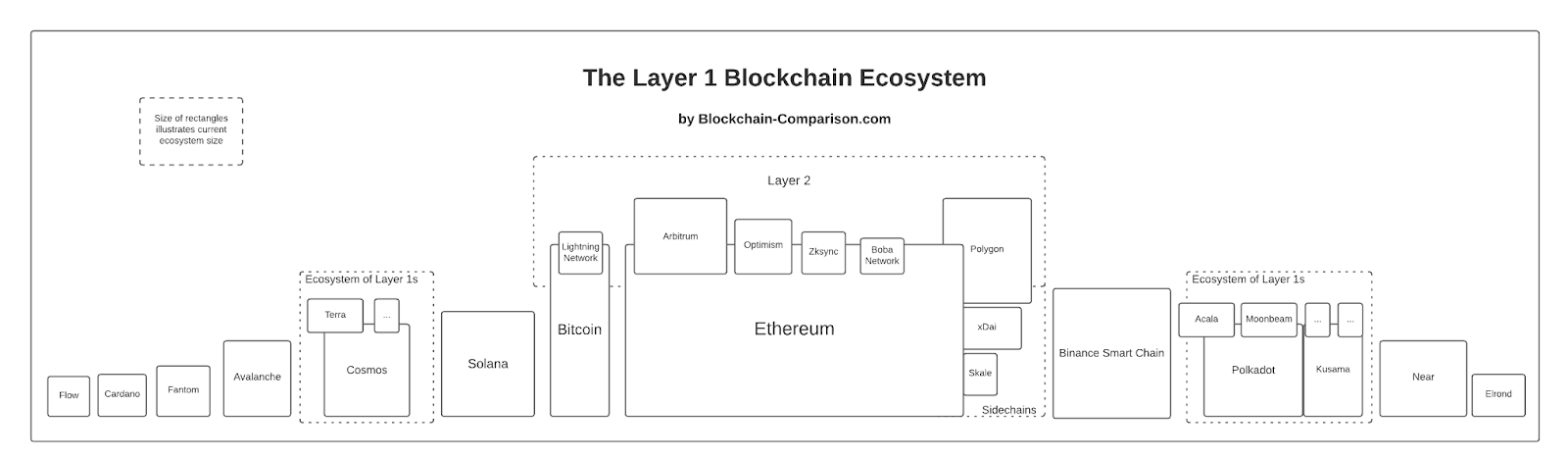

You may wonder what I mean by “Layer 1” (L1). Bitcoin, Ethereum, and the other emerging blockchains are considered L1s, because they are the core/foundational blockchain. Layers 2s (L2s) have helped Ethereum scale recently. These are other blockchains built on top of Ethereum that process a bunch of transactions, and send only one transaction to Ethereum L1 for confirmation. L2s reduce the load on L1s, thus helping blockchains scale to more transactions per second.

Ethereum is also in the middle of a major update to its L1 chain as it transitions to Ethereum 2.0. Its new software architecture will feature 64 sharded chains that connect to a main beacon chain. The sharded chains will process transactions in parallel to one another, thus ramping up the transaction per second that Ethereum 2.0 can handle. Also, Ethereum 2.0 will transition its consensus mechanism from Proof of Work to a new mechanism called Proof of Stake (PoS), which we’ll talk more about in the next section. Developers estimate Ethereum 2.0 will handle 100,000 TPS thanks to its sharded chain architecture plus PoS consensus mechanism.

Ethereum launched in 2015 as the first smart contract blockchain and, despite competitive Layer 1s, has remained the second largest cryptocurrency by market cap to this day. Ethereum’s dominance can be measured in more than market cap – tens of billions of dollars worth of crypto is transacted on it every day, and Ethereum attracts over 4000 active monthly developers, which is the most of any layer 1 blockchain.

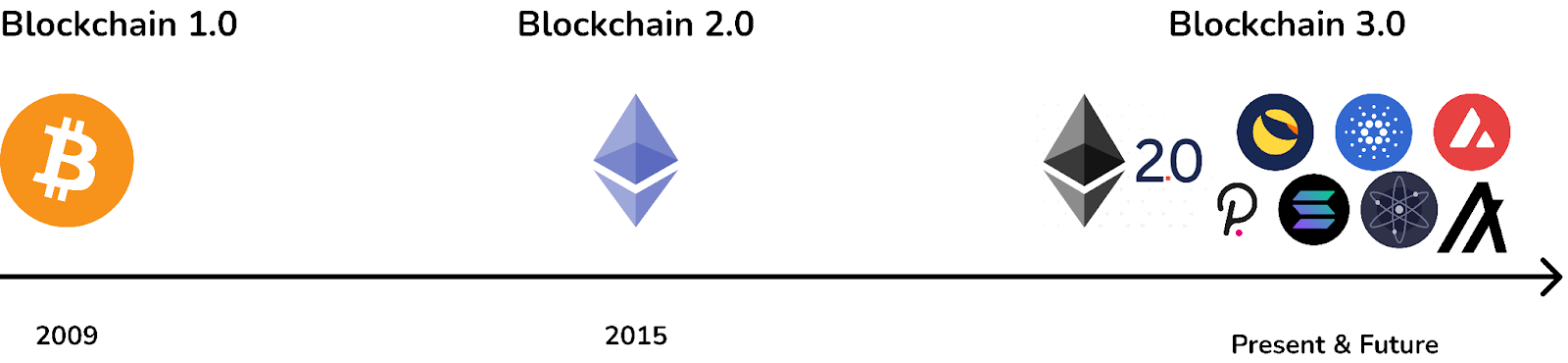

Having said all that, other competitive layer 1 smart contract blockchains are sprouting up, and building up significant developer and end-user communities. This landscape of emerging layer 1 blockchains brings us to the present moment. If Bitcoin is blockchain 1.0, and Ethereum blockchain 2.0, then we are now in the era of blockchain 3.0. These emerging layer 1s seek to solve problems in blockchain scalability and interoperability, each with a unique design philosophy and cultural ethos.

2.3 – Other Emerging Layer 1s & the Blockchain Wars

Right now we are witnessing rapid growth in the emerging layer 1 blockchain landscape. Ethereum is undergoing major reconstruction in its transition to Ethereum 2.0, and competitive layer 1 blockchains intend to steal market dominance from Ethereum, as well as support the next wave of Web3 adoption with scalable and interoperable technologies.

Layer 1 blockchains are like nationstates. They all have their own economies powered by their native cryptocurrency. Each blockchain attracts its own developer community, who then build out a Web3 ecosystem on top of the blockchain, thus attracting end-users. These are the “blockchain wars” that you may have heard people talk of. The emerging Layer 1s are sometimes referred to as “Ethereum-killers”.

At the end of the day, blockchains are competing for more end-users. Metcalfe’s law stipulates that the more users in a network, the more valuable the network is. This is also known as “network effect”, and we can look at a familiar example as to why this is. Users sign-up to Facebook because there are already billions of users with Facebook accounts. They want to go where their friends and family already have accounts. In other words, they are attracted to Facebook’s existing network effect. It wouldn’t be hard to copy Facebook’s code, and deploy TravisBook, but it would be extremely difficult to get any user adoption, because Facebook is already the dominant social network.

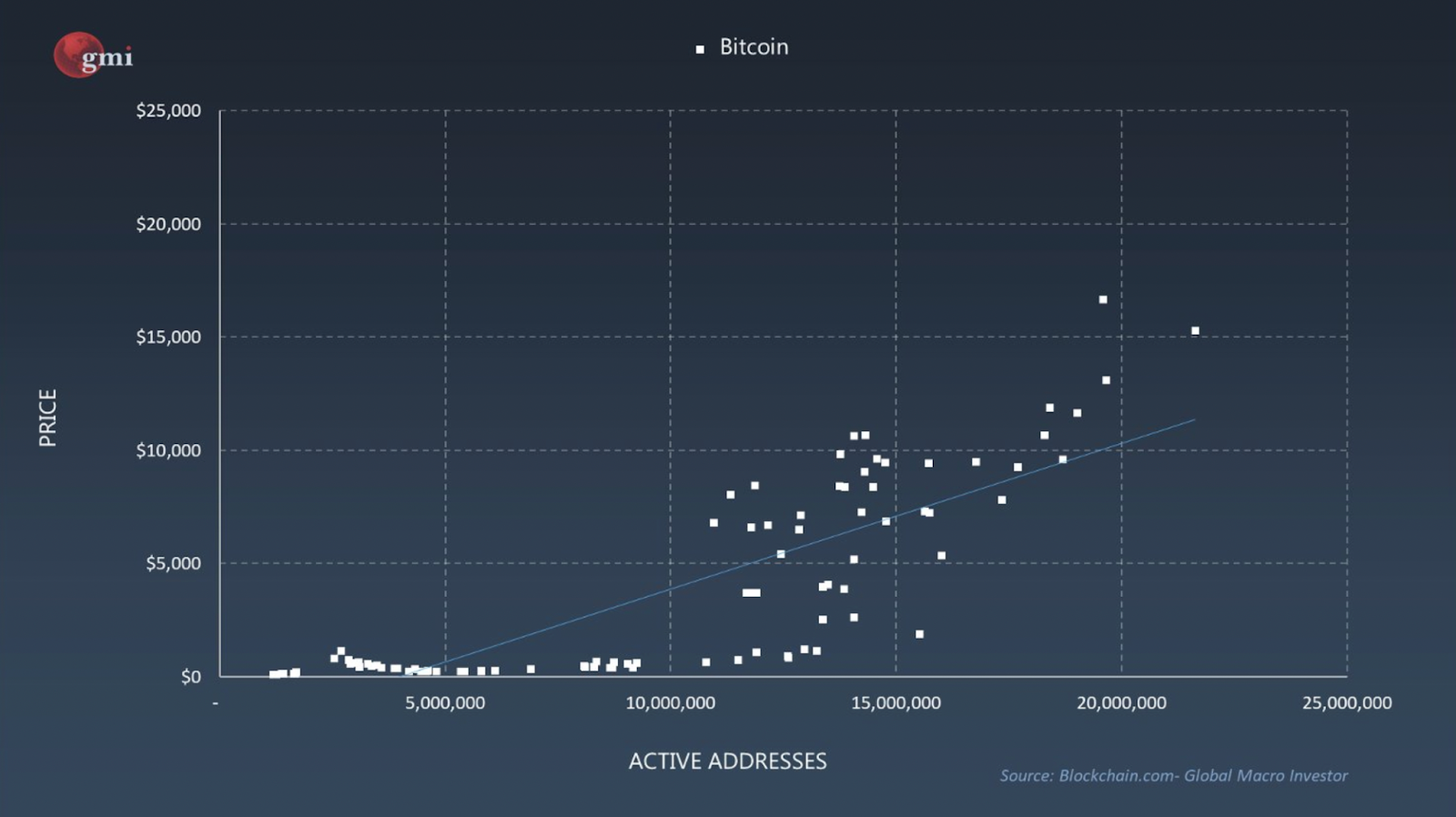

This relationship appears to be true for blockchain networks. Macro investor Raoul Pal has shown the market cap of a crypto network is proportional to the square of active wallet addresses. This phenomena of winner-take-all exists everywhere in the tech landscape – think of Facebook, Amazon, Google, Apple, and Netflix. How many people do you know use a search engine alternative to Google? This proliferation of layer 1 blockchains, and their Web3 ecosystems, looks a lot like the internet tech boom in the 90’s. The lesson we learned from that is that 99% fail, and 1% take all.

All of this leads to something unfortunate about Web3 culture, “chain maximalism”. People want the blockchain they are invested in to be the winner. This explains why crypto Twitter, and the culture in general, can feel toxic and divisive. It’s just something to understand as a product designer, that blockchain developers and end-users have financial incentives to oppose other blockchains, and Web3 ecosystems.

But, it likely won’t be as cut and dry as one single winning blockchain. As we’ve already seen Bitcoin and Ethereum both serve two different use-cases. Bitcoin’s design is optimized for decentralized digital currency, and Ethereum is a platform that runs decentralized applications. We will likely live in a multi-chain future as blockchain design does not appear to be a one-size fits all. Maybe people will have their preferences like PC versus Mac, but more likely blockchains will be designed with specific use-cases in mind.

For example, a blockchain built for decentralized social media doesn’t need the greatest security guarantees, but needs to process hundreds of millions of transactions per second. Whereas, another blockchain might be responsible for trillions of dollars locked in decentralized finance protocols, and need to be trusted by large public institutions. This blockchain would presumably need better security guarantees than the social media blockchain.

The Layer 1 blockchain landscape is quite varied in terms of design philosophy and software architecture; however, all Blockchain 3.0 Layer 1s have several things in common.

- Proof of Stake consensus for energy-efficiency

- Increase transaction throughput to scale blockchain to more users

- Improve blockchain interoperability and avoid siloed ecosystems

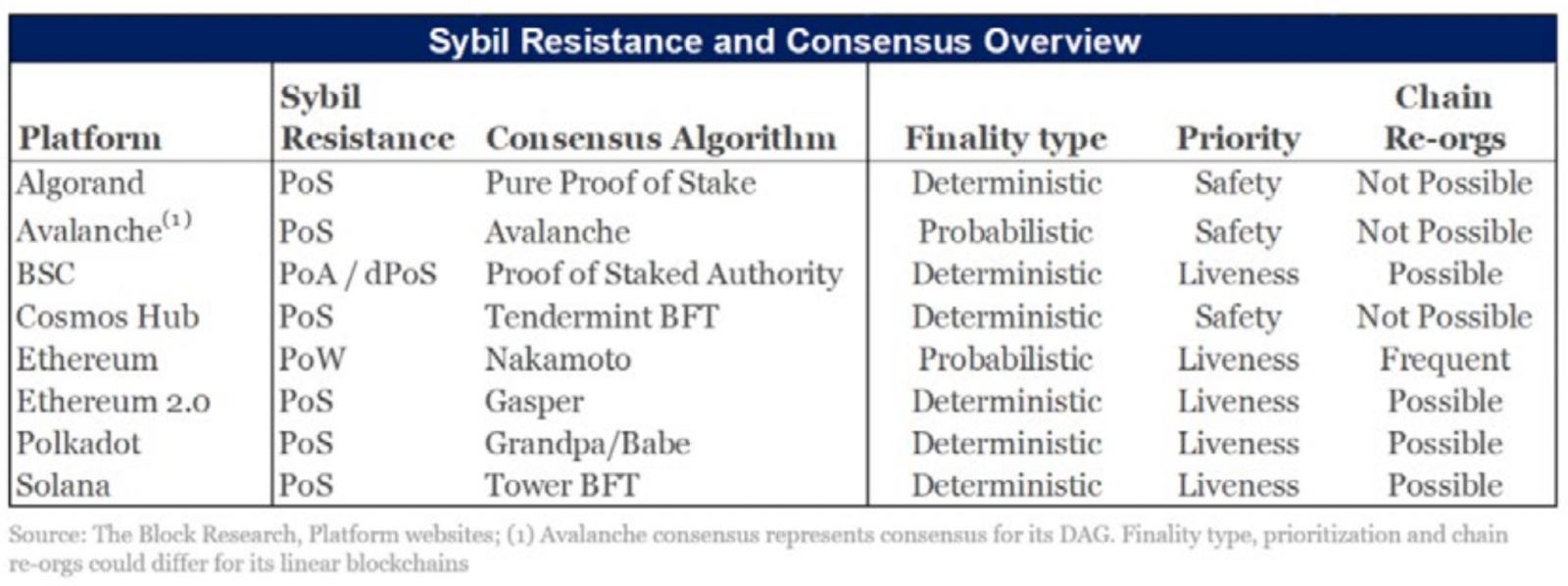

Let’s pause on Proof of Stake for a minute. Proof of Stake is the consensus mechanism of all emerging Layer 1s, and is an innovation on Bitcoin’s Proof of Work consensus. In PoW, nodes spend electrical energy in order to create blocks; whereas, in PoS, nodes stake the Layer 1s native cryptocurrency in order to create, and vote on, blocks. This is like posting a security deposit in order to participate as a validator node. The more crypto a node stakes, the greater chance that node will have to participate as a validator node, and earn block rewards. That’s the carrot – to earn block rewards – but there’s a stick as well. Staking crypto makes it so that nodes have skin in the game. Nodes can have their stake slashed if they do something that undermines the blockchain. Nodes with the most at stake will be chosen as the validator nodes, and work to maintain the blockchain.

PoW and PoS are not intuitive and the reader still may have confusion about how consensus mechanisms work, but don’t worry about understanding these concepts fully. Consensus mechanisms are highly technical topics that play on multiple fields like game theory and computer science. We discuss Proof of Stake here because it unlocks a brand new investment vehicle for Web3 end-users. Users can delegate their crypto to validator nodes, and share in the block rewards these nodes earn for maintaining the blockchain. Users earn dividend payments proportional to the amount they delegate, and this is similar to traditional passive income assets like bonds. Staking has the potential to disrupt the financial sector as Proof of Stake Layer 1 blockchains grow in prominence.

So now we’ve discussed the brief, 13-year history of blockchains starting with Bitcoin, moving to Ethereum, and ending with the emerging Layer 1s currently vying for position in the Blockchain 3.0 era. Interestingly, the vast majority of end-users will not care which blockchain their dApps are running on. Currently, users don’t care which database technology (MongoDB, MySQL, etc.) their Web 2 application uses, and it won’t be any different for Web 3. That’s assuming that the underlying blockchains don’t impose UX limitations on them like high network fees, slow transactions, low staking yield, or a siloed ecosystem with no cross-chain communication.

2.4 – Comparing Layer 1 Blockchains

As Web3 product designers it’s important for us to understand the blockchain landscape in order to decide which ecosystems to build products in. Let’s finish by discussing a framework for comparing Layer 1 Smart Contract Blockchains developed by The BLOCK Research. The research compares Layer 1s across 4-dimensions:

- Technical Design & Performance

- On-Chain and Ecosystem Data

- Tokenomics and Monetary Policy

- Team and Fundraising

Technical design and performance can be broken into network architecture, consensus mechanisms (e.g. PoW vs PoS), and performance metrics like transactions per second and time to finality. Blockchain design is still highly experimental. Of course, founding teams are in search of the design that results in the most favorable performance metrics. Many will fail, some will succeed.

On-chain and ecosystem data is good for assessing the health, and/or growth of a Layer 1 blockchain. For example, we can objectively say that Ethereum is still the most dominant smart contract blockchain because it has the greatest daily transacted value, largest developer network, and most value locked in its DeFi protocols. Number of active wallet addresses is another important metric. Remember, wallet addresses can be used to predict the value of a blockchain’s cryptocurrency.

Each Layer 1 has its own native cryptocurrency, controlled by its own tokenomic model. Some are fixed-supply (like Bitcoin), and others are inflationary, although there is more nuance here. For example, Ethereum is implementing a policy where a portion of ether network fees are burned. Some believe this will actually make ether a deflationary asset. Also, native cryptos have utility value as well. Users can delegate their crypto to earn staking rewards, and often token-voting is used to participate in a Layer 1’s governance process.

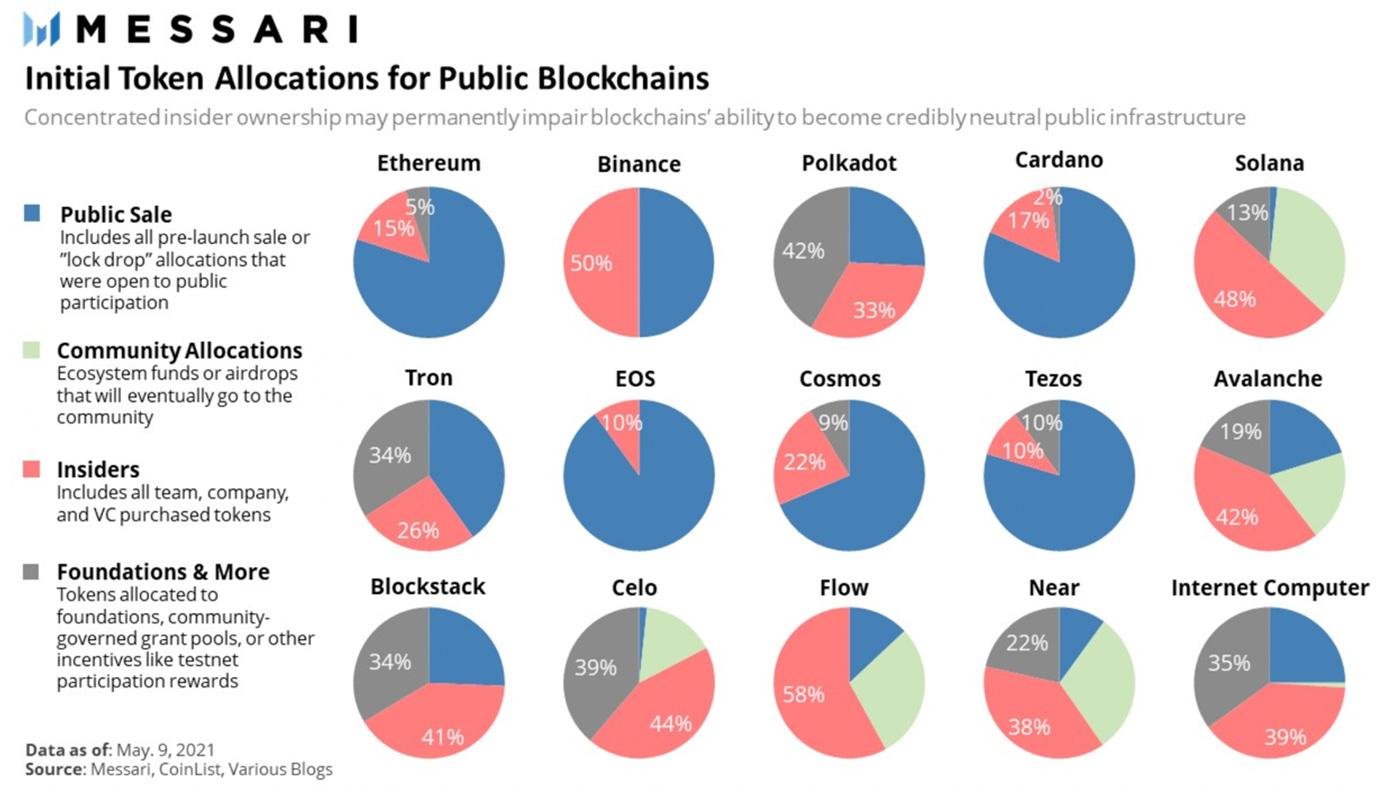

Finally, Layer 1s are being built out by teams of people who influence the ethos and design philosophy of the blockchain. And these teams need to be funded. This brings up a controversial point. Blockchain projects will often hold fundraising token sales, which VCs are increasingly participating in. This calls into question decentralization and the idea of fair launches when VCs own a significant portion of a blockchain’s native token.

There was a lot of mention about native Layer 1 tokens in this article; however, you probably know there are tens of thousands of crypto tokens in existence today, and wonder where they all come from. These other Web3 tokens belong to dApps and secondary protocols that build on top of the blockchain. Indeed, smart contract Layer 1 blockchains give developers the ability to deploy their own tokens with application-specific utility. Also, these bleeds into the topic of crypto art and NFTs, which are a specific type of token on the blockchain.

3 – Web3 Tokens as Incentive Mechanisms

Software protocols define the rule set for how a software system will operate. In the case of blockchain, the blockchain protocol defines how the nodes communicate, and come to consensus, with each other in order to form a functioning cryptonetwork.

Software protocols have been crucial in the development of information technologies. Billions of users everyday rely on internet protocols to access the web. These internet protocols dictate how networked computers request and share information with each other. Let’s take a look back at how these protocols developed, and where we are currently in terms of the development of the internet as a whole.

The internet is simply a network of connected computers. Once computers are physically connected in a network, software protocols standardize how these computers share data with one another. This includes rule sets for locating other computers on the network, sending data packets to a desired location, and checking that messages were received and correctly interpreted. These internet protocols can be broken into four layers.

- Hardware protocols

- Internet Protocol (i.e. IP)

- Transmission Control Protocol (i.e. TCP)

- Application Protocols (e.g. HTTP)

Hypertext Transmission Protocol (HTTP) is an important application protocol. HTTP defines how a computer requests data from, and serves data to, another computer. A common example is for a computer to request an HTML file from a web server (using an HTTP GET request) in order to view a web page on its internet browser.

This HTTP GET request then gets passed down one layer to the Transmission Control Protocol (TCP), which tells the computer how to break the message into smaller data packets that will be sent one by one to the web server. TCP is also used by the web server receiving the data packets in order to assemble the data packets back into the original message.

The Internet Protocol (IP) ensures that the data packets reach their intended destination. Before sending the HTTP GET message via TCP, the IP wraps data packets with an IP address corresponding to the web server. This is like the “To:” field on a mail envelope. Finally, hardware protocols convert the data packets into electrical signals that get transmitted through the internet’s physical infrastructure (e.g. cables, modems, routers).

On the other end, the web server will send back an HTML file using the same HTTP and TCP/IP process described above. Now you have a rough idea of how the web functions with a set of open-source internet protocols. These protocols were developed by independent researchers and non-profit organizations, and haven’t been modified much since the mid-1990’s. All of the web products we enjoy today would not exist without these internet protocols.

3.1 – Internet History from Web1 to Web3

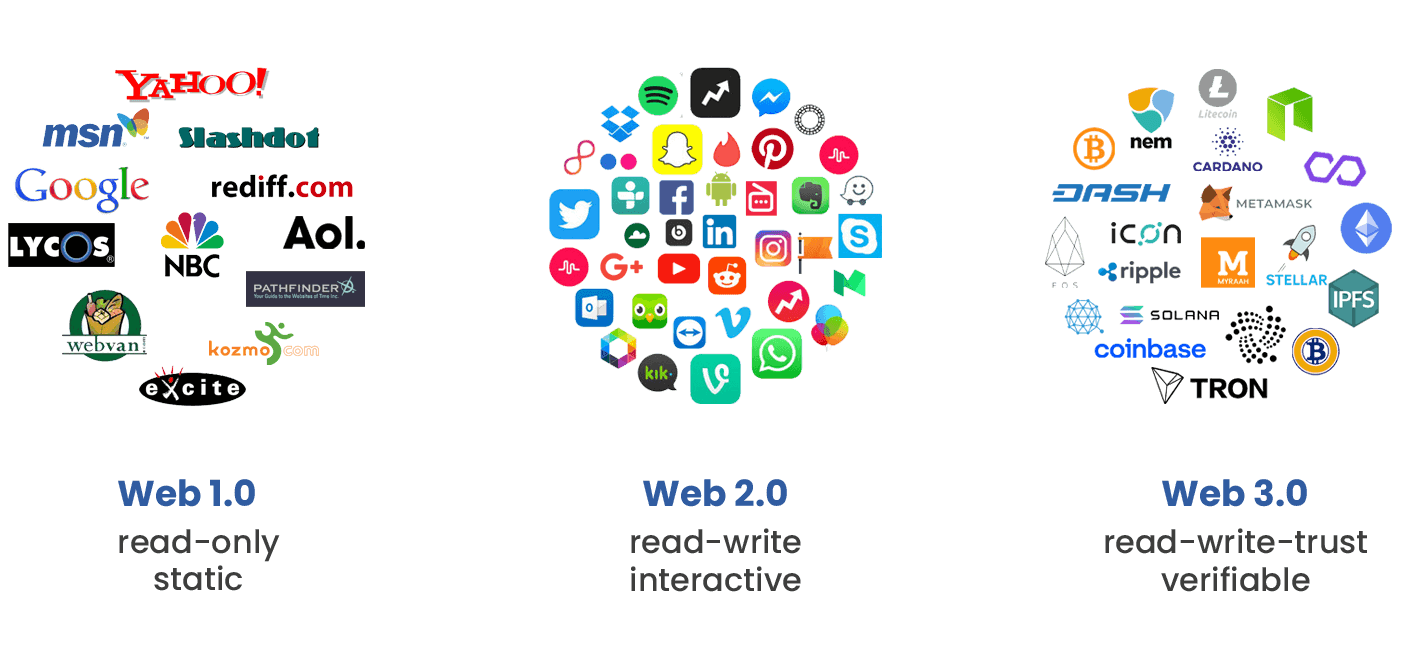

This is a good point to talk about the evolution of the internet. We can break the internet’s development into three phases: Web1, Web2, and Web3.

Web1 is characterized as “read-only” because only a few entities published content for consumption by many. The internet was thought of at this time as a digital encyclopedia. Users accessed static web pages containing text, images, and hyperlinks; however, there was little interactivity for end-users other than consumption.

This brings us to Web2, which is also referred to as the “social web”. Online communities and identities began to emerge at this time. Web2 is especially characterized by social media platforms, and the idea of user-generated content. Now everyone had the ability to create content, build a social network, and react to the posts of others (e.g. like and share buttons). The web went from a few content creators to billions. If Web1 is considered “read-only” then Web2 can be considered “read-write” for the average user. Centralized web platforms attracted users with large networks and simple user experiences.

This has ended in a winner-take-all dynamic. There are several monopoly-like companies, such as Google, Amazon, Apple, and Facebook, that largely control how the internet is experienced by end-users. For example, users must agree to the terms and conditions of these centralized companies if they want to participate in the dominant social network. Also, Web2 companies have the rights to all the user data generated on these platforms, which they mine and sell to advertisers. Roughly 98% of Facebook’s revenue is generated in this way. It’s a strange idea that we’ve become accustomed to – that users who join a network, and increase the value of that network with their presence and activity, capture little, if any, of the value they create.

Additionally, large user bases act as an economic moat that protect Web2 companies from competition, making these platforms cautious of third-party development, and product integrations. This incentivizes Web2 companies to close-off their ecosystems, which stifles innovation. For example, Apple is able to reject applications from launching on its app store for any number of reasons, one of which being competitive risk. And, even when it accepts applications, Apple takes a hefty 30% cut from the application’s revenues. Of course, third-party developers are paying for the privilege to launch on a platform with a reach of over 1 billion iOS users. Still, one wishes for something better than a system that extracts value from its end-users, and regards third-party development coolly, if not with open-hostility.

To recap, going from Web1 to Web2, we went from open-source internet protocols, intended to decentralize information sharing, to monopoly-like, centralized social networks that limit end-user choice, and third-party integrations. Web3 can remedy the current issues with Web2. Web3 users can literally self-custody their data, identity, and other digital assets with cryptographic wallets. And, developers can now choose to build applications on neutral, open-source Web3 platforms (i.e. blockchains). Web3 removes rent-seeking middlemen and connects users directly to the applications they want to use. If things change, they can pick up, and move to another ecosystem that better suits their needs, without the loss of data or other digital assets.

One of the major innovation’s of Web3, and something important to wrap your head around as a Web3 product designer, is that Web3 aligns incentives better than the current system. Developers, end-users, and cryptonetwork service providers (i.e. nodes) are all incentivized to work towards the same goal – the growth of the cryptonetwork. This is all made possible by Web3 tokens.

3.2 – Design Principles of Web3 Tokens

Tokens native to a cryptonetwork incentivize nodes to secure, and maintain, that cryptonetwork. These nodes can be thought of as network service providers. They dedicate their resources to provide a decentralized blockchain database for dApps to build on top of, and are rewarded with that cryptonetwork’s native token.

Additionally, native tokens are staked by these nodes to ensure that they act according to the best interest of the cryptonetwork. This secures the cryptonetwork from attack because stakes can be slashed. The cryptonetwork is also protected from denial of service attacks by requiring users to pay for their usage of the cryptonetwork with its native token. This makes spamming the network with unnecessary transactions prohibitively expensive.

In other words, the native token coordinates, and incentivizes, globally distributed, independently-acting nodes to maintain the blockchain, while at the same time protecting it from attack. This is all kind of complicated. You may notice this is unnecessary in the world of Web2 because companies cover the cost of the centralized databases their applications run on. But, as we already talked about in the previous section, there are hidden costs with centralized gatekeepers who have unilateral control over the platform, and its data. Simply put, tokens make possible the decentralized, open, and neutral properties of Web3.

Think back to what we learned about internet protocols. They were developed over 30 years ago by independent researchers and non-profit organizations, and haven’t changed much since. In the beginning, before the enormous commercial value of the internet was realized, it was difficult to get funding to build out the protocols. Now, protocol developers can create a cryptonetwork and hold on to a portion of the native token. If the protocol provides value, and is adopted, then the token price will increase in value, because the token is required to use the cryptonetwork in the first place (see above). Also, the founding team can sell off some of the tokens to fund initial, or ongoing, development. Thus, Web3 tokens provide a direct value capture, and funding, mechanism for open-source protocols.

This brings us to the next point – Web3 tokens help bootstrap cryptonetwork adoption. Remember, networks are proportional in value to the number of users in the network. Facebook is much less compelling with only 100 users, and AirBnB just isn’t that useful with only 100 hosts. So it’s difficult to get things off the ground; however, cryptonetworks can reward its early-adopters – whether that be developers or end-users – with its native token. If the network succeeds then the early-adopters profit greatly, rewarding them for the value they provided to the network early on. Also, now that they are token holders, and have a financial stake in the network, early-adopters are incentivized to help grow the network through word of mouth, or social media promotion.

Think about the internet as divided into two layers: the protocol layer (e.g. HTTP, TCP/IP, etc.) and the application layer (e.g. Facebook, Instagram, etc.). In Web2, all of the value accrues to the application layer, which has led to some of the most valuable companies in the world today. Remember there was no effective way to capture value from open-source protocols until Web3 tokens came along.

The fat protocol thesis posits that value will consolidate at the protocol layer in the Web3 era. As dApps, built on these Web3 protocols, go mainstream and attract hundreds of millions of users, the protocol’s native token will increase in value. This is because the native token is required to use the dApps – a classic example of utility tokens, discussed in the next section. An increase in token price signals a growing ecosystem, which will attract more developers to build out additional functionality on the blockchain, which will attract more end-users. Web3 tokens are responsible for positive feedback loops like this.